Some of the largest pension funds in the world are paying an average of 86.3 basis points in total annual investment costs, with 24 per cent of these fees made up of transaction costs, according to new research.

Cost analysis service CEM Benchmarking has found that 19 of the world’s largest pension funds, with over £2tn in combined assets under management, are estimated to be paying 20.2 bps in yearly transaction costs. Two UK funds took part in the survey.

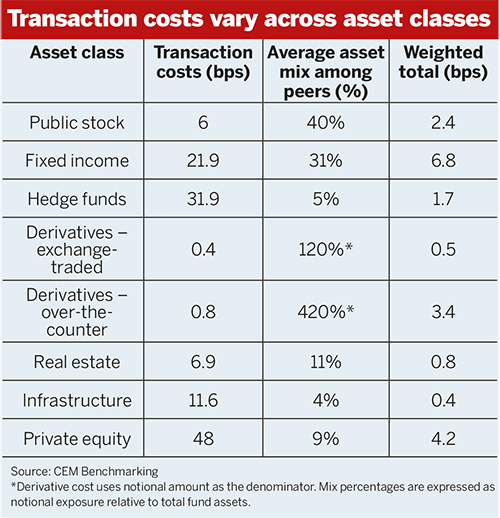

In public markets, the relatively high trading volume of fixed income meant it had the highest median transaction costs, at 21.9 bps. The median asset turnover of traded fixed income over a year came to 74 per cent, compared to 40 per cent for public equity.

There are funds, and managers of funds, for whom turnover is their secret sauce

James Knowles, Novarca

While those surveyed said they have the ability to include transaction cost limits as part of a manager selection process, they admitted that they are more likely to impose an asset turnover limit instead.

Difficult to get full picture of costs

In January 2018, the implementation of Mifid II saw asset managers forced to separate execution services and research costs. Meanwhile, the Financial Conduct Authority's asset management market study has led to additional disclosure standards for both managers and pension funds.

There evidently remains, however, the need to improve the state of cost transparency for pension funds. According to John Simmonds, CEM Benchmarking principal, not one fund was able to provide a “complete picture across all of the asset classes”.

He added: “Historically there’s been some reluctance on the part of the fund management industry to supply this kind of information."

The UK is trailing other nations in the push to boost transparency. Dutch pension funds have been required to disclose their costs, including transaction costs, since 2015.

However, Mike Heale, principal at CEM Benchmarking, admitted that there is no evidence to suggest that rising transparency has helped the Dutch to negotiate lower asset management fees.

“Costs are neither inherently good nor bad,” he argued. “What matters the most,” he added, is whether funds are “generating value in relation to what you’re spending”.

Do not overly constrain managers

The role of transactions in generating overall cost has also shone a light on the value provided by managers relying on high turnover. According to CEM Benchmarking, there is a 127 per cent turnover rate of all fixed income in the 75th percentile of funds surveyed.

James Knowles, managing partner at cost specialist Novarca, observed that Mifid II has so far helped to reduce asset turnover, but has failed to quell suspicions that managers are excessively generating transactions.

“There are funds, and managers of funds, for whom turnover is their secret sauce,” he said.

“If you said, all of a sudden, ‘You can’t do that’, you might find that that constraint comes back to bite you. Returns go down, the manager blames the constraints,” he added.

Investors will need support

The FCA’s Institutional Disclosure Working Group, a key outcome of the watchdog's market study, could yet deliver a boost to pension schemes struggling to understand their costs.

The IDWG has now submitted its template for cost disclosure to the FCA, although they have not yet been released for schemes and managers to use.

The working group has requested regulators, advisers and institutional investors take responsibility for improving investor understanding of costs.

It has also recommended that “a new body or group should be created by autumn 2018 to curate and update the framework”.

Chris Sier, chair of the IDWG, said that a 'help desk' would be necessary to help some investors navigate the cost transparency data within the template.

Transparency worries hinder flows into active quant strategies

More than half of institutional investors are wary of using quantitative investment strategies, with a perceived lack of transparency registering at the top of investors’ concerns, according to new research.

“If we release the templates without that organisation having been formed, and without the help desk having been put together, we will end up with chaos,” Sier said.

He observed that trade volume and the quality of the traders themselves are the two material components to establishing transaction costs.

“This is why both the absolute cost, but also the best execution, are being measured by Mifid,” he said.

One of Mifid II's objectives is to establish whether traders are achieving the best possible outcome for clients when conducting transactions, either via execution venues or over-the-counter.