Royal Dutch Shell has introduced a new financial education hub for employees, as members of the company’s pension fund show appetite for online communications.

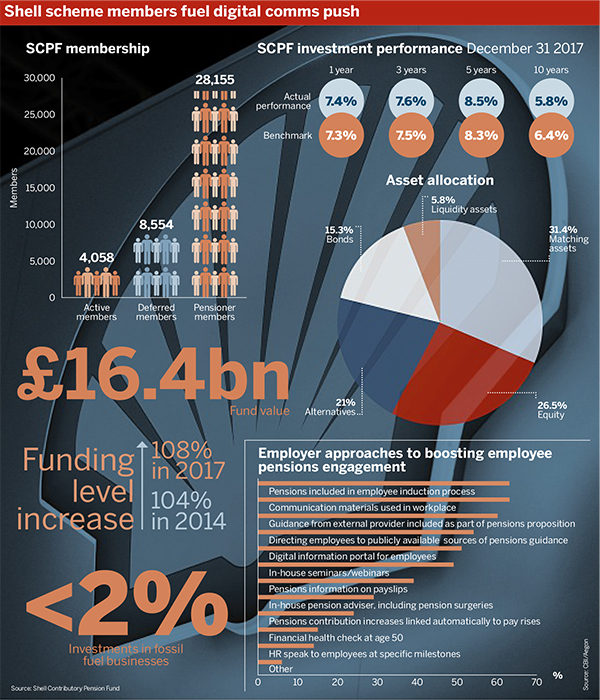

The trustees of its defined benefit pension scheme, which recently reached a funding level of 108 per cent, have also written to scheme members outlining their focus on climate change risk.

In order to explore further what people are actually feeling, and what the reasons for the responses are, you need them in the room

Karen Partridge, AHC

The Shell Contributory Pension Fund surveyed members in 2017 to find out what they wanted from pensions communications.

Sixty-nine per cent of respondents said they would prefer to receive information via email, a result that the scheme welcomed due to its desire to move from paper-based to digital communications.

The trustees have directed members to the company’s new financial education hub, which gives employees access to a financial education programme.

They have also communicated the pension scheme’s approach to the impact of climate change, highlighting that its holding in shares of fossil fuel companies make up less than 2 per cent of the scheme.

New hub launched

Engagement with pensions is driven by a mixture of employees’ behavioural biases and the commitment shown by employers to boosting engagement, according to research.

In March, Aegon and the Confederation of British Industry found that two thirds of businesses said further educating employees about the benefits of saving through a workplace pension would improve engagement with pensions.

Shell introduced a new financial education hub earlier this year, according to its November 2018 SCPF member newsletter, the Source.

It described it as “a one-stop-shop for employees to access a widened and improved financial education programme”.

In addition to career-stage and topic-based financial education sessions, the company has added several new services, including a dedicated helpline.

The programme is designed to help employees with a range of financial issues, including planning for retirement. Members also have access to information on pensions taxation and the annual allowance.

Employer role crucial

Kate Smith, head of pensions at Aegon, said employers have an important role to play when it comes to financial education.

“They have regular contact with employees… and employers do tend to be a trusted source of information,” she said.

A financial hub hosted on a workplace intranet is a good way of providing information, support and guidance, Smith said.

With thousands of UK employees, Shell is a particularly large company. Experts said smaller businesses with fewer resources may not have the means to develop their own financial education resources, but can leverage other sources.

Darren Laverty, partner at Secondsight, said: “If employers don’t feel they have a big enough budget to fund their own offering, they could look at what they may be able to [get] from their pension providers.”

He added that many mainstream providers will include robust communication tools or portals within their product offering.

Employers might also come to the conclusion that spending a fraction of a per cent on a financial wellbeing portal or better pension communications is worth it in the context of ensuring that their contributions, which are a significantly larger expense, have the desired effect, Laverty said.

Talk to members

Shell’s pension fund has been pushing electronic communications for several years. In 2016, it began requesting email addresses from members as it took its first step towards electronic communications.

A 2017 survey of scheme members found that 69 per cent of respondents said they would prefer to receive information via email.

“This is great news, as we want to move the SCPF’s communications from paper-based to digital for as many members as possible,” the newsletter stated.

When asked which of the communications members had received this year that they found most useful, most pensioner members said it was their pension increase letter.

“The results of the survey are extremely useful for understanding what you, our members, are most interested in, and we’ll use these results to design future editions of the Source, as well as our other communications,” the newsletter added.

Karen Partridge, head of client services for UK and Australia at communications specialist AHC, said surveys can help reveal what members want.

“In order to explore further what people are actually feeling, and what the reasons for the responses are, you need them in the room really. You need to have a conversation, or at the very least you need to be on the phone to them,” she said, adding that focus groups are often helpful.

We’re monitoring how all this affects the oil industry in general – Shell in particular – we’re actually more interested in the longer-term, say over 10, 20 plus years

Tim Morrison, SCPF

She said moving communications online is often motivated by “savings to be made in terms of print and postage”, particularly where there is a large audience. Online communications also allow trustees to use analytical tools to measure member engagement and views.

Shell scheme looks at climate risk

The scheme has also used its latest newsletter to highlight its focus on climate change risk.

“There’s increasing interest in how climate change will affect major asset holders, such as pension funds,” said new chairman of the trustee board Tim Morrison in a video published on the scheme website this month.

“It’s also generally reckoned that the financial impacts of climate change will be material, but quite what form they take and over what timescale is still very uncertain,” he added.

Morrison said that how society responds to climate change affects the fund both via its impact on the strength of Royal Dutch Shell as the sponsor, and the investment strategy.

“We’re monitoring how all this affects the oil industry in general – Shell in particular. We’re actually more interested in the longer-term, say over 10, 20 plus years, than in the very short term, because the current covenant is so strong,” he said.

Morrison noted that the investment portfolio’s holding in fossil fuel businesses is small as a proportion of its total assets; according to the pension scheme newsletter, it is less than 2 per cent.

“What we’re really interested in is the impact on the global economy as a whole. We’re interested in how this translates into the returns on different types of assets. This is a very complex question, and we’ll be devoting a lot of time to this over the years to come,” he said.

Shell’s scheme was one of 25 large funds that the Environmental Audit Committee wrote to in February, asking how they manage the risks climate change poses to pensions.

The EAC categorised the SCPF as “engaged”, meaning it is considering climate issues and is making some progress.

The EAC said this group acknowledged climate change as a risk, but often saw it as one of the many environmental, social and governance factors they had to contend with. Policies might be in place, but there was less evidence of significant activity around implementation of climate risk management.

Shell was one of the large companies targeted by a consortium of investors – including the Church of England pensions board – earlier this month, due to their significant role in energy intensive sectors, as well as their high greenhouse emissions.

Ralph McClelland, partner at law firm Sackers, said these types of campaign show that pressure is building on schemes to engage with climate change.

“The more that there is a recognised direction of travel, the more information is published, the more public scrutiny is put on the risks that are associated with climate change and their relevance to trustees as asset owners, the harder it is – I think – for a trustee to say that they can reasonably disregard those risks”.

Shell sees funding level boost

In a message featured in the SCPF newsletter, Morrison highlighted that the scheme is in “good financial health”, with an improvement in the level since the last valuation.

The newsletter explains to members that the statutory funding objective aims for 100 per cent funding of the technical provisions.

The SCPF was 108 per cent funded on this basis as at December 31 2017, up from 104 per cent at December 31 2014. The estimated solvency level, the amount of benefits the scheme could secure on winding up, was 73 per cent at December 31 2017.

The scheme’s actuary explained in the newsletter that, since the previous valuation, the scheme’s liabilities increased due to a sharp fall in real interest rates, offset in part by a reduction in life expectancy assumptions based on national population trends and experience of the fund’s own members.

However, the assets have also increased, with strong investment returns over the period, which has seen the funding level rising to 108 per cent.

Hugh Nolan, director at Spence & Partners, said that getting to a funding level of 100 per cent is all well and good on a technical provisions basis, but it is “always nice to have a little extra buffer in”.

If a scheme is funded at something like 110 per cent and is aiming towards buyout, “you can afford to have a little bit of a pump on the investment markets and try and get yourself to buyout, knowing that the downside is not going to kill you on the contributions because you’ve got a safety margin to play with already”.