With most defined benefit pension funds having an eye on the ‘endgame’, and for many this ultimately meaning buyout, a wariness towards locking assets up into illiquids that are hard to sell is not surprising.

Trustees worry they may find themselves in a position where buyout seems achievable, based on the pricing in the bulk annuity market and on their asset values, only to find a buyout is scuppered by illiquid assets they can neither exit nor persuade the insurer to take off their hands.

So in these latter years of many pension funds’ lives, should they only focus on liquid markets?

Opportunities to invest in private credit are available for most schemes and the credit spreads on offer can be attractive

At the Society of Pension Professionals, we think the answer is no — particularly when it comes to credit exposure, but possibly even elsewhere. To do so reduces opportunities to diversify and gives up potential yield opportunities.

Don’t give up on illiquid credit

It would be dangerous to buy longer-dated private market credit issues, even highly rated ones, assuming the insurance company with which a scheme is transacting will take these on.

Insurance companies are particular about their credit exposures, having their own approved lists and exposure limits. The future state of the secondary market is also an unknown, and in illiquid markets you never want to find yourself forced into a quick sale.

However, in an age of liability-driven investment, pension funds are able to divorce their interest rate hedging from their credit exposure.

Despite widening in 2020 in reaction to the pandemic, credit spreads later narrowed relatively quickly and are back around the levels they reached before the financial crises.

Yet there certainly remain structural challenges. For example, the public, highly rated, long-dated sterling credit market has a significant weighting to utilities that face the challenge of transitioning to a green economy.

Shorter maturities help

Holding credit of a shorter maturity reduces the credit risk. Of course, there is still event risk, but there is far less time for any structural decline in credit worthiness to jeopardise repayment.

Additionally, holding more credit at shorter maturities increases the contractual cash flow delivered by the investment, which can be used to pay pensions. Having this potential for cash flow matching reduces the risk of having to be a forced seller in down markets.

There is good rationale for shorter-term credit, and if a pension fund invests in shorter-dated credit then it might be expected to hold it to maturity, even if it is targeting buyout.

This makes the lack of a secondary market a non-issue and critically challenges the exclusion of illiquids from many pension portfolios.

Credit where credit is due

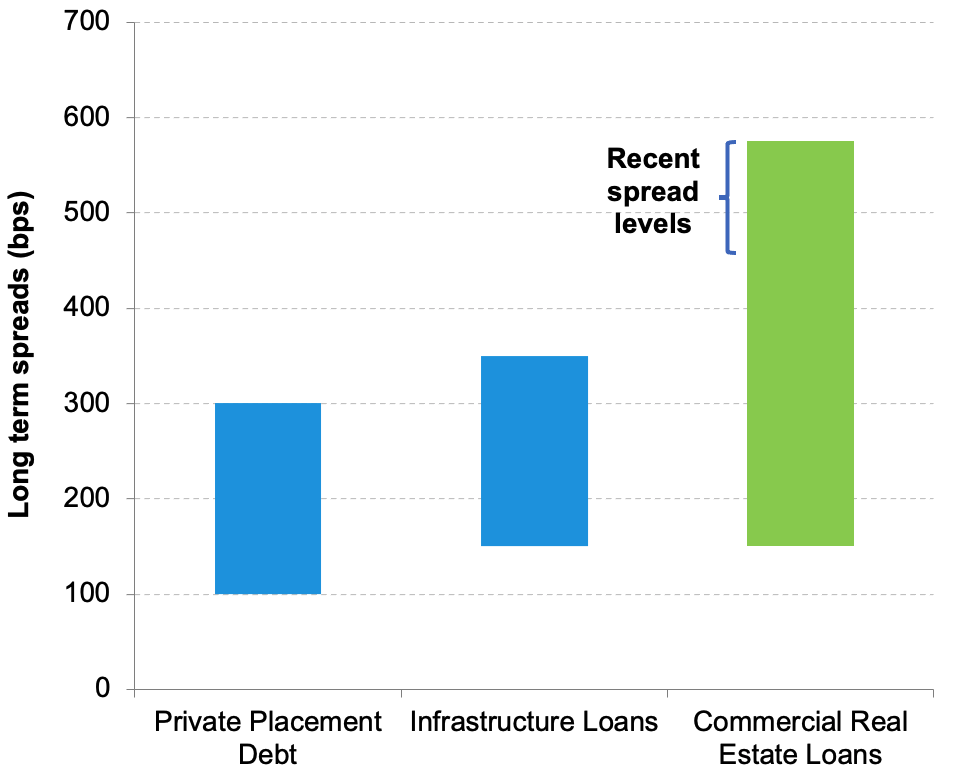

There has been a substantial growth in private credit markets with various types of borrowers. For example, as well as corporate borrowers, there are commercial real estate debt and infrastructure debt, and the return opportunities in these private markets can be significantly better.

An additional credit spread of more than 1 per cent might be seen in private debt when compared with a public market bond with equivalent risk, for instance. Add to that the fact that the recovery rates are quite likely to be higher too, and the investment case is hard to ignore.

How attractive commercial real estate loans are faring

Source: Abrdn. Gross of fees

While some private market debt can be very long-dated, such as infrastructure or social or university housing, there are shorter-dated private market loans too.

Maturity profile

In scoping the maturity profile of a portfolio of private market credit, as well as the possibility of reaching buyout early, trustees will need to consider possible extension options in a loan contract, and consider maximum term as their constraint instead.

But even considering this, opportunities to invest in private credit are available for most schemes and the credit spreads on offer can be attractive.

However, trustees do not have to stop at shorter-dated credit. Very long ground rents or infrastructure debt, even though not publicly traded, are likely to still be very marketable in the future.

Where such assets do offer attractive characteristics with attractive yields, trustees should not rule them out — as long as they can plan their exit strategy.

Natalie Winterfrost is a member of the Society of Pension Professionals’ investment committee