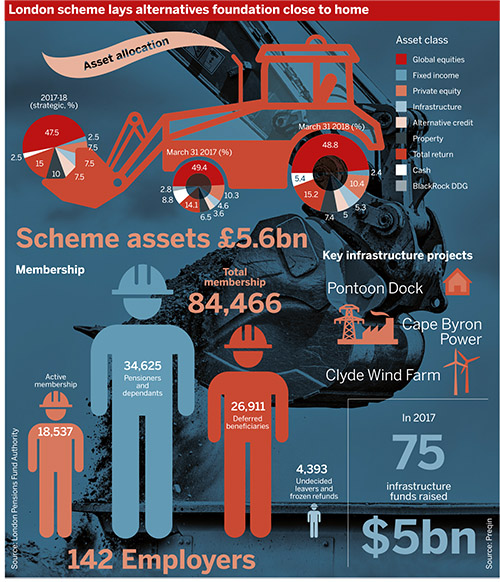

The London Pensions Fund Authority will cut the ribbon next year on the Pontoon Dock, a residential property project incorporating 154 high quality privately rented homes and 82 affordable homes available for rental or shared ownership.

The £5.6bn scheme has a £13.4m stake in the east London development, which has been in progress since 2014.

The average pension scheme allocation to property in the UK stands at 3 per cent, according to Mercer.

The pools at the moment are purely there to implement the strategic decisions of the underlying funds

Nick Buckland, JLT Employee Benefits

Pontoon Dock is the latest in the LPFA’s portfolio of property and infrastructure projects.

In 2013 the scheme invested in Cape Byron Power, an Australian biomass-fired power station, via an infrastructure pool.

Last year, it announced an increase in its stake in the Clyde Wind Farm, where it is invested alongside infrastructure platform GLIL.

Across Europe, 4 per cent of schemes are invested in listed infrastructure, while 3 per cent have allocations to unlisted infrastructure.

Robert Branagh, managing director at the LPFA, said that the fund is interested in renewable investment opportunities in the private rental sector.

LPFA joins other LGPS funds in the housing market

The Local Government Pension Scheme has had a notable impact in residential housing over the past few years.

The £4.9bn Nottinghamshire County Council Pension Fund recently added £10m to its local property fund and expanded the geographical area in which it invests.

Last year, the £21.3bn Greater Manchester Pension Fund was close to finalising a series of impact investment deals, worth about £100m, which are expected to build roughly 2,000 local homes.

According to Branagh, the LPFA board approved an update to its strategic allocation at the end of 2017, which entails greater allocations to property, infrastructure and credit.

“That’s against a background of, for a lot of LGPS, rising funding levels and quite healthy finances in the last 12 months,” he said.

As of the scheme’s last actuarial valuation at March 31 2016, the LPFA was 96 per cent funded.

“We believe that, being pension schemes, we have long-term commitments to our members and to our funding, and therefore having holdings in infrastructure is also a long-term, not a quick turnaround-type of, investment,” he added.

This is primarily achieved via investment in the £1.3bn GLIL infrastructure platform, which is comprised of the LPFA, GMPF and the Northern pool.

The Northern pool, which has £46bn of assets under management, is made up of the GMPF and the West Yorkshire and Merseyside pension funds.

Property is easier to access than infrastructure

Unlike most pension schemes, the LPFA is not limited to investment via managers and pools, and is directly involved with the Pontoon Dock project, which is being developed alongside residential property business Grainger.

In addition to its planned homes, Pontoon Dock will include shops and provide greater access to the Thames Barrier Park.

“We’re interested in other opportunities like that, looking forward,” Branagh said.

Rodney Lumpkin, managing director of private market strategies at SEI, observed that the property investment universe is far greater than that of infrastructure.

“It’s much more institutionalised today. The assets are a little bit smaller in many cases so the managers have a lot of things from which to choose,” he said.

Institutional infrastructure investment is often global, according to Lumpkin, which often involves multiple currencies and regulatory requirements.

“When you start looking at infrastructure, the issue becomes [that] the assets are much larger in most cases, or you have a minority position… there’s the dollars needed to own something,” he added.

Infrastructure is more compatible with DB than DC

The LPFA has indeed gone global with its infrastructure investments, having purchased Cape Byron Power out of receivership alongside the Local Pensions Partnership.

The LPFA’s investment in the company was conducted via the LPP’s alternative investments manager Local Pensions Partnership Investments. It sits in LPPI’s global infrastructure fund, the pooling vehicle for the infrastructure assets of LPPI’s clients.

Cape Byron Power is made up of two 30 MW biomass-fired power stations. Together, they form one of Australia’s largest renewable base load generators. They burn sugar cane waste and wood.

Richard Butcher, managing director at trustee company PTL, said that defined benefit schemes view infrastructure as a solid growth prospect by way of an illiquidity premium.

He advised trustees examining exit routes for their schemes to avoid the asset class.

“You don’t really want to buy an illiquid investment, or an investment that gives its best return over a 10 or 20-year period if you’re planning to buyout in the next five to 10 years,” he said.

The PLSA chairman added that property is popular among defined contribution schemes. Infrastructure is rarer due to its relative incompatibility with daily pricing.

Daily pricing or dealing, is used in DC to enable investors to transfer in and out of funds at will using up-to-date valuations for those assets.

“Some of the very large DC schemes will use infrastructure because they don’t have to worry so much about daily dealing, because they can just daily deal into other places, or out of other places, and balance the books later on. Their timeline is very long,” he said.

Investors do not want fossil fuels

In April, GLIL was relaunched under a regulated structure. It was formed in 2015 by the LPFA and the GMPF with an initial £500m investment.

The £1.3bn infrastructure platform has carried out approximately £600m of investments.

In March 2016, Scottish energy company SSE sold 49.9 per cent of Clyde Wind Farm to a joint consortium of GLIL and renewable infrastructure fund Greencoat UK Wind, for £355m.

Under the terms of the agreement, GLIL and Greencoat UK Wind’s stake would be diluted to 30 per cent upon the wind farm’s completion in June 2017. SSE would retain 70 per cent.

In August 2017, SSE announced an additional 5 per cent acquisition in the wind farm by GLIL and Greencoat UK Wind for a cash consideration of £67.8m, before costs, taking their joint stake to 35 per cent.

On May 8, SSE announced that the consortium had exercised an option to buy a further 14.9 per cent, for a cash consideration of £202m before costs, lifting their stake to 49.9 per cent.

Jason Cogley, managing director at specialist fund manager Fiera Infrastructure, heralded the advantages of investing in unlisted infrastructure projects.

“You have the added advantage of not being correlated with the equity market, which over the last 18-24 months has been quite volatile,” he said.

The CBOE Volatility Index, or Vix, which measures the expected volatility of the US stock market, closed at 12.48 on August 30 2018. In comparison, on August 30 2017, the Vix closed at 11.22.

Environmental, social and governance considerations are also key to infrastructure investment, according to Cogley, who expressed uncertainty about the long-term prospects of fossil fuel assets.

Investors have also demonstrated a desire to move away from fossil fuels. “We’re actively steering away from coal, oil and refined petroleum,” he said.

Pooling is not deciding investment strategy

Local government pooling is well underway, and schemes are using the framework to access new opportunities in property and infrastructure.

Last month, Pensions Expert reported that the £3.1bn Rhondda Cynon Taf Pension Fund has set in motion plans to nearly double its property exposure and its alternative assets to 25 per cent from its present position of 5.4 per cent.

Nick Buckland, senior investment consultant and LGPS adviser at JLT Employee Benefits, played down the role of pooling in setting LGPS investment strategy.

“The pools at the moment are purely there to implement the strategic decisions of the underlying funds,” he said. “Further down the line, who’s to say, but at this stage I think that the pool is very much an implementation tool rather than an influencer of strategy.”

Infrastructure investment is a cornerstone of the pooling effort that is taking place across LGPS. At the time of its announcement, “it struck me that actually it shouldn’t have needed a government push for funds to invest in it”, Buckland said.

“In fact it didn’t need a government push. Investments in infrastructure were being made by LGPS funds anyway,” he added.

In 2015, the average local authority pension scheme had a 11.2 per cent allocation to alternatives, according to UBS Asset Management. 10.5 per cent of this capital was tied up in infrastructure, on average.

Rhondda Cynon Taf approves plan for alternatives

The Rhondda Cynon Taf Pension Fund has agreed to wind down its lofty equity exposure in favour of new allocations to absolute return bonds and infrastructure.

Buckland observed that the structures used to funnel investment into infrastructure, be they via pools, partnership or direct involvement, depend highly upon the size of the scheme involved.

He predicted that the GLIL model will soon be used by other LGPS funds to access infrastructure. “It gives funds the opportunity to invest into assets that they may have previously had to do via pooled structures with fund managers,” he said.