The UK government has an ambitious climate and environmental agenda and is set to issue its first green gilt in September 2021, with at least one more issue before the end of the year.

The funds raised will finance clean transportation, renewable energy, energy efficiency, pollution prevention and control, living and natural resources and climate change adaptation, according to the UK government’s Green Financing Framework published on June 30 2021.

Green bonds in the UK present an opportunity for trustees to invest in green initiatives but have the protection of a Treasury-backed bond

Penny Cogher, Irwin Mitchell

All worthy objectives, but should pension funds take the plunge and invest in these gilts and other green bonds? By investing in green bonds, “investors have probably the most direct way to finance the reduction of greenhouse gas emissions”, says Daniel Karnaus, senior portfolio manager at Vontobel.

He adds: “Actively integrating [environmental, social and governance] risks into the investment process improves the long-term risk-return characteristics of portfolios.”

As interest in the area is growing, this can result in a ‘greenium’, but it need not mean sacrificing performance relative to investing in ‘regular’ bonds.

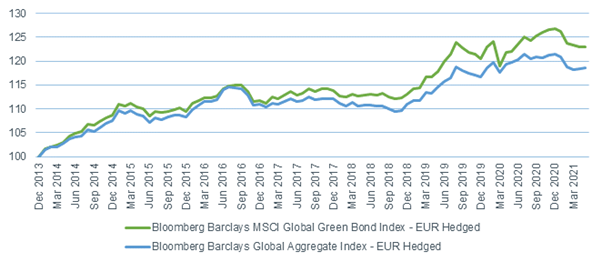

Penny Cochrane, investment research consultant at Hymans Robertson, notes: “The Bloomberg Barclays MSCI Green Bond Index (EUR hedged) has outperformed the Bloomberg Barclays Global Aggregate Index (EUR hedged) by 0.5 per cent per annum since the inception of the former in January 2014, and this outperformance is more significant over a one-year period at 1.6 per cent.”

Green bonds have outperformed since inception in January 2014

Source: Bloomberg

Grey still beats green

Yet support was lukewarm for green finance at a poorly attended Pensions and Lifetime Savings Association ESG Conference live text chat session entitled ‘Getting into green gilts’. Indeed, the lack of ‘chat’ indicated that going green is not yet at the top of trustees’ agendas.

But one trustee was prepared to stick his head above the parapet. Derek Scott, chairman of trustees at Stagecoach Group Pension Scheme, said he was not interested as “yields were unattractive”.

Jonathan Lawrence, ESG analyst at Legal & General Investment Management, to a certain extent backed this view: “We have seen some evidence of a greenium for green bonds, and investors need to be conscious of how demand and supply dynamics influence this in both the primary and secondary market.

“There has also been some evidence of the greenium reducing as supply reaches a critical mass; for example, the greenium has on average been more pronounced in US dollar and [sterling] denominated bonds compared with issues in the euro,” he adds.

On green bonds more generally, Lawrence says: “We do not believe pension funds should necessarily be investing in green bonds over vanilla bonds from the same issuer.

“The sustainable debt market has helped to encourage greater disclosure and therefore transparency for investors. However, it is not clear that these bonds deliver any true impact above vanilla bonds, while exposure to the overall balance sheet of the issuer remains the same.”

Worst-case scenario

There are several key risks for investors. Joshua Palmer, head of fixed income and ESG research at Willis Towers Watson, notes: “Currently, green bond labels are non-binding from a legal and regulatory perspective. In a worst-case scenario, this could result in misallocation of funds if not properly monitored.”

He adds: “Independent industry bodies are now producing standards for issuers and investors. Green bonds have also been offering less compensation than their non-green counterparts, demonstrating that the risk reduction from sustainability initiatives may be priced in already, or that the overwhelming demand for green bonds has made the pricing too expensive.”

Palmer also points to the “high sector concentration in green bond issuers in government/related financials, utilities and transport firms, which could increase volatility in asset owner portfolios”.

He says: “While we believe the issuance of these bonds is a step in the right direction, we continue to prefer a broader mandate assessing all bonds, both green and non-green.”

One of the main barriers is the fiduciary responsibility to not invest in something that has a lower expected return.

Despite the conventional wisdom that green bonds which carry a greenium are not viable investments, Zhoufei Shi, investment strategist at Cardano, says: “This underestimates the forward-looking returns of these bonds, given our view that demand will increase and hence greenium can increase further (ie, outsized price appreciation), while also potentially offering a better risk-reward trade.

“The volatility of these bonds may in fact be lower in the future than the grey equivalent due to the holding pattern of investors in green versus grey,” he adds.

On the regulatory side, Penny Cogher, partner at Irwin Mitchell, points to the Pensions Scheme Act 2021, which adds new provisions into the Pensions Act 1995 on climate change risks.

“Green bonds in the UK present an opportunity for trustees to invest in green initiatives but have the protection of a Treasury-backed bond,” she says.

“They may be useful investments to assist trustees in meeting the new requirements under the Pensions Scheme Act 2021 in relation to climate change risk and governance.”