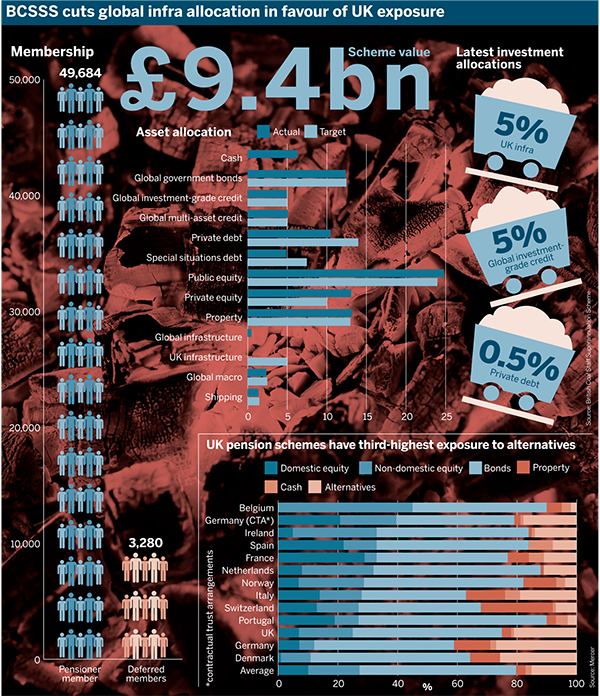

The British Coal Staff Superannuation Scheme has introduced a new allocation to UK infrastructure and increased its exposure to private debt, as part of its focus on assets that provide diversification, good return prospects and high cash yields.

The £9.4bn defined benefit pension scheme has also invested in global investment-grade credit.

Target allocations to several asset classes within the pension fund’s portfolio, including global infrastructure, public equity and private equity, have been reduced.

The committee has looked to broaden the investment universe to identify assets that provide both high cash yields and good return prospects

Kate Barker, BCSSS

The scheme invests in a wide range of assets, many of which are illiquid, meaning they cannot be sold quickly to generate cash to meet benefit payments to members.

To address challenges related to managing a portfolio with high levels of illiquid assets, the scheme has strengthened its internal investment team.

Infrastructure is often seen as an attractive opportunity for schemes looking for diversification and long-term returns.

The asset class can include renewable energy projects, telecoms, hospitals, schools, roads and ports.

The amount of investment reported by UK asset managers into infrastructure grew to £40bn by the end of 2017, from £29bn reported at the end of 2016, according to a survey of The Investment Association’s members.

Real assets, which include infrastructure, remain one of the most popular forms of alternative assets among European pension schemes, Mercer’s 2018 European Asset Allocation Survey found.

The multi-employer DB Baptist Pension Scheme, for example, recently introduced an allocation to global infrastructure.

The British Coal Staff Superannuation Scheme also has a global infrastructure allocation, but over the year to March 31 2018 it reduced its global exposure in favour of UK infrastructure.

Strong investment markets have helped the scheme generate high returns from across a range of asset classes. The BCSSS has been able to take advantage of these good returns, and as a result its funding position has improved, according to documents from the scheme’s annual meeting on October 18.

However, Kate Barker, chairman of the committee of management of BCSSS, noted that the scheme’s expectations of future returns on assets is lower than they have projected historically.

Furthermore, low interest rates have led investors to compete for assets that provide high cash yields, which has driven up their price.

“As a result, the committee has looked to broaden the investment universe to identify assets that provide both high cash yields and good return prospects”, she said.

That is the reason why the scheme has allocations to property, private credit and ships. “We have recently also committed a significant allocation to UK infrastructure,” Barker added.

This target allocation makes up 5 per cent of the scheme’s investment portfolio, the latest BCSSS annual report shows. It states that UK infrastructure “is expected to provide a diversified form of return when compared to more traditional asset classes such as equities”.

As at March 31 2018, the scheme had £40m invested in UK infrastructure with asset manager Dalmore Capital.

The scheme reduced its target allocation to global infrastructure from 2 per cent to zero. It reduced its public equity target allocation to 24 per cent from 30 per cent. It also cut its private equity allocation by 2.5 percentage points to 10 per cent.

The pension fund has annual benefit payments in excess of £600m. Barker noted that these payments out of the scheme are greater than the income it receives from the assets, meaning that the fund has to sell assets over time to pay the pensions.

“Therefore, our funding strategy has to have regard to the high return targets and the high cash payments,” she said.

UK environment attracts infra investors

Anish Butani, director, private markets at bfinance, noted that most UK pension funds have sterling-denominated liabilities that are linked to the retail price index.

“As such, investing in UK infrastructure provides a way of hedging that liability by investing in underlying assets that are GBP denominated and are generally well correlated to UK inflation. That would be the primary attraction of a UK fund investing in the local market,” he said.

Many investors are concerned about political and regulatory risk when making investment decisions. They are also looking to spread their diversification. However, “the UK remains attractive to many investors for its historically regulatory environment and the integrity of the English legal system”, Butani noted.

He added that, “given the heightened concerns around political risk when investing in infrastructure globally, some investors may prefer to play closer to home”.

Butani also highlighted the need for trustees to consider the lack of liquidity and long duration of the investment.

“The very nature of investing in infrastructure demands vigilance; if the project fails to deliver there will be no quick and easy exit, unless the investor is willing to endure a substantial loss of capital in exchange for a rapid exit,” he said.

Illiquidity challenges prompt team changes

Many of the assets that the BCSSS invests in are illiquid. Barker noted that managing the portfolio with high levels of illiquid assets brings some new challenges.

As a result, under the scheme’s new chief investment officer Mark Walker, “we have strengthened our internal investment team to recognise these challenges, including bringing in individuals with experience in these new investment areas”, she said.

The committee has reviewed its risk management framework, with a greater focus on cash flows to and from investments, the management of illiquidity and the need for growth. It is also considering environmental, social and governance factors.

Alan Pickering, chair of professional trustee company Bestrustees, said: “If the trustees want to major on ESG… or major on particular asset classes – perhaps property, real assets – then they may well bring someone on to the staff who can implement trustee decisions in these areas or provide a link between the generalist trustees and the specialised external market sector.”

Private debt opportunities

The scheme has increased its target allocation to private debt to 14 per cent from 13.5 per cent.

Pickering highlighted that the private debt market is increasing in a number of countries, “so availability is one attraction, but just because something is available doesn’t necessarily mean that it’s appropriate for everyone”, he said.

Many schemes are looking for new sources of income, Pickering said, noting that private debt is a potential source of that income.

There may also be an illiquidity premium associated with that private debt, he added. However, schemes have “got to be careful that that illiquidity premium doesn’t inhibit their ability to move on to the next stage of their journey, whatever that next stage might be”.

The BCSSS has also introduced a new 5 per cent allocation to global investment-grade credit. The allocation has been split equally across two managers – Wellington Management and PGIM Fixed Income.

David Rae, managing director and head of strategic client solutions at Russell Investments, noted that UK credit represents about 5 per cent of the global investment-grade credit opportunity set.

“There have always been significant diversification benefits to investing in offshore credit markets and these remain today,” he said.

Consider currency risk when going global

Rae added that there is a broader industry representation across global markets. Furthermore, Brexit uncertainty increases the risk of sterling credit at the current time.

“Global markets offer access to a much broader array of credit and fixed income opportunities, this includes across emerging markets, securitised debt, and loans,” he said.

“Many investors have looked to reduce the exposure to longer-duration investment-grade credit in favour of floating rate or shorter duration instruments, which are less susceptible to losses from rising rates,” Rae added.

He noted that the cost of hedging currency risk needs to be considered by pension schemes, particularly for trustees looking to invest relative to a sterling liability.

Simeon Willis, chief investment officer at consultancy XPS Pensions, said that when it comes to investing in global investment-grade credit, “you need to make a decision on how much you’re going to allocate to the different regions” and have a methodology for allocating to different markets.

Schemes need to manage currency risk, and “you also need to think about how the role of some emerging markets investments play in, because a lot of them will be investment grade”, Willis added.

Trustees should be aware of the nature of the interest rate risk in different markets. “If you invest in the US, and you’re a UK pension scheme, if interest rates change differently in the US to how they do in the UK, that will impact your bond investment differently,” he said.