More than one hundred academies and colleges participating in the Hertfordshire County Council Pension Fund have been sent erroneous actuarial reports. These were subsequently used in the preparation of their own financial accounts.

Committee meeting minutes indicate an error in the fund’s actuarial report that led to overstated annual asset returns and an overstatement of Hertfordshire’s funding level.

The mistake happened because incorrect quarterly asset return figures submitted to consultancy Hymans Robertson had not been reviewed and approved by “senior officers”, the minutes state. A council spokesperson confirmed the actuary is not at fault.

Hertfordshire has since introduced controls to ensure that a senior officer in the team will now review and sign off returns. An accompanying audit trail will be provided to the actuary detailing the returns for the relevant time period.

We were made aware of the erroneous actuarial reports shortly after we had submitted our financial statements

University of Hertfordshire

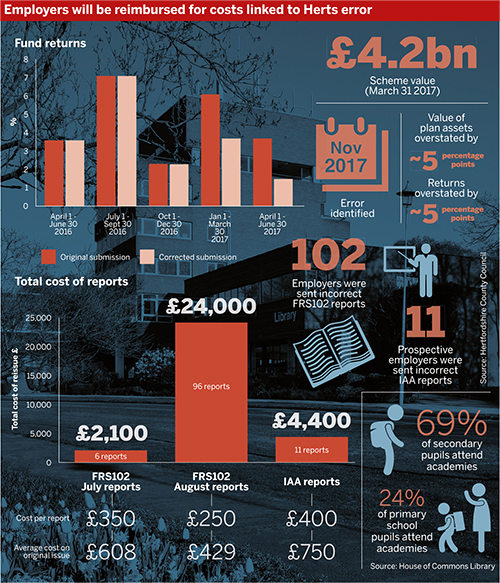

The actuarial reports were sent to 102 employers, who will be reimbursed for audit and accounting costs linked to the error.

A decision has not yet been reached on whether the pension fund or the administering authority will provide the funds for this compensation.

Some returns must be estimated

Academies and colleges prepare their accounts under Financial Reporting Standard 102. The fund’s actuary produces FRS 102 reports for all employers in the fund upon request, using actuarial assumptions, membership data and investment returns from the 12 months before the reporting date.

Officers in Hertfordshire’s finance department are responsible for supplying the actuary with asset valuations and returns for the fund’s investments on a quarterly basis. This information is taken from reports developed by its custodian, BNY Mellon, and its investment consultant, Mercer.

There are time-lags in the availability of asset valuation data, and these periods do not coincide with the end of all employers’ financial calendars.

Of the employers, 96 operate on an August year-end basis and 6 close their financial year at the end of July.

This means the actuary regularly has to value returns on a ‘roll-forward’ basis. For example, where it receives quarterly returns data up to June 30 it will estimate July returns for organisations with a July 31 year-end.

The council used the wrong reports

Information on fund returns for Q4 2016-17 and Q1 2017-18 was drawn by a council officer from the wrong investment consultant performance period reports, according to a committee document.

Returns for the quarters were overstated, as the recorded data mistakenly related to previous quarters, which listed higher asset returns.

“Internal controls within the team responsible… were not sufficient to identify the incorrectly entered data,” a committee document reads.

The quarterly return for the period January 1 to March 31 2017 was originally misstated at 6.1 per cent. This has been revised downwards to 3.7 per cent.

The following quarter’s return was first recorded at 3.7 per cent. The corrected return stands at 1.5 per cent.

These figures were sent to the fund’s actuary, which used the numbers when producing annual returns for the affected employers’ FRS 102 reports.

For those with financial calendars running until the end of July, returns from August 1 2016 to July 31 2017 were calculated at 15.7 per cent, when they should have been recorded at 10.7 per cent.

The 96 employers with August year-ends initially had returns from September 1 2016 to August 31 2017 set at 16.6 per cent. These have since been lowered to 11.6 per cent.

Error has had a material impact

Overall, actual returns and total returns were overstated by about 5 percentage points. Numerous figures within the FRS 102 reports were subsequently incorrect, including the fair value of plan assets, which was also overstated by around 5 points.

Analysis conducted by the actuary revealed that this last error “would likely lead to a material effect on employers’ balance sheets and profit and loss statements”, according to a committee document.

“The issue was identified in November as a result of a funding update which looked inconsistent with the expected position,” said Barry McKay, head of Local Government Pension Scheme actuarial at Hymans Robertson and consulting actuary for the Hertfordshire County Council Pension Fund

“There was no impact on the plan assets,” he said, adding that “the returns are only used to roll-forward and estimate the employer assets”.

All employers in receipt of erroneous FRS 102 reports were notified by email on December 4. The council issued updated reports by December 6.

The University of Hertfordshire was among the organisations for whom this discovery came too late.

“Unfortunately we were made aware of the erroneous actuarial reports shortly after we had submitted our financial statements to the Higher Education Funding Council for England in December 2017,” a university spokesperson said.

“Our external auditors are fully aware of this error, as is our audit committee, and we will be making a financial adjustment in next year’s accounts to reflect it,” the spokesperson added.

The mistake was especially untimely for academies, which risk incurring fines for the tardy submission of accounts.

Every year academies are required by the Education and Skills Funding Agency to provide their financial statements to the Department for Education by December 31.

Prospective employers have also been hit

‘Initial asset allocation reports’ were sent to 11 employers looking to join the fund. These reports set out the liabilities at the point of transfer, and the value of assets to be allocated to employers in order to meet these liabilities.

The same error meant that these reports overstated initial funding levels. The recipients were notified of the mistake on December 5 and new IAA reports were issued by December 14.

Had the mistake not been recognised it could have led to an insufficiently high contribution request from the local authority, according to Mark Vincent, partner at consultancy Quantum Advisory.

It could also have affected employers exiting the scheme. “If they thought they’d paid off their debt and the debt was calculated to be too low, then the local authority might have gone back to them saying, ‘We asked for too little, give us some more money’”, he said.

Employers have received updated reports

Within the FRS 102 reports, the projected defined benefit cost, recognised as ‘interest income on plan assets’ was also overstated. This led to the ‘total net interest cost’ within profit and loss being too high.

The difference here was “likely immaterial to most employers” at approximately 0.125 per cent, according to the council.

The actuary has since provided all affected parties with updated initial asset allocation and FRS 102 reports.

A council spokesperson said: “All impacted bodies have been informed and revised reports issued to those employer bodies.”

As of February 7 2018, the financial impact of the mistake stood at £33,323. It cost £30,500 to reissue all the reports, and £2,823 was spent on reimbursed audit and accounting fees.

Hertfordshire has tightened its controls

The council has revised its process for submitting quarterly returns data to its actuary. The process “now includes a reconciliation between performance data from BNY Mellon and Mercer to ensure consistency prior to submission”, according to committee minutes.

The actuary will cross-reference these data with supporting evidence from the custodian and the investment consultant.

Hounslow drops Capita and heads for West Yorks

The £991m London Borough of Hounslow Pension Fund will enter into an administrative partnership with the West Yorkshire Pension Fund following the imminent conclusion of its contract with third-party administrator Capita.

All data produced by the council’s finance department are now reviewed by its senior accountant or finance manager before submission to the actuary.

“Any performance, training and learning points raised by this issue have been taken forward by the council under its internal procedures,” a spokesperson for the council said.

The spokesperson confirmed that the individual responsible for the mishap still works for the council.