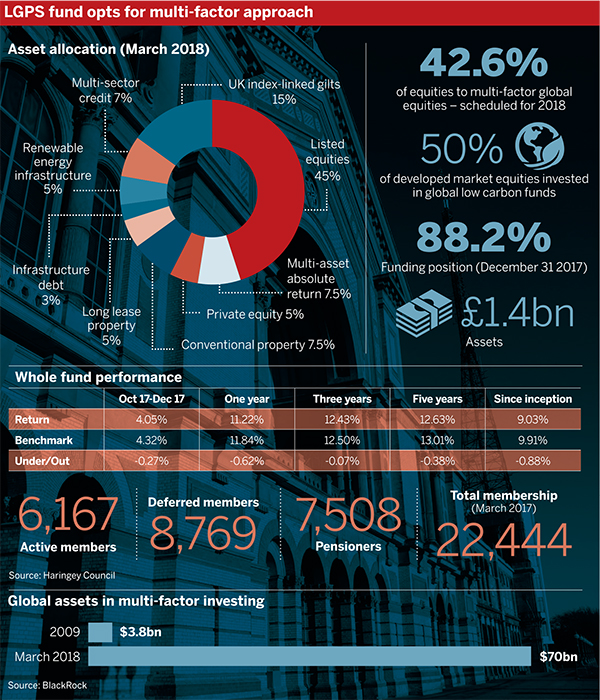

The London Borough of Haringey Pension Fund has agreed to convert nearly half of its equity allocation from a passive fund into a multi-factor global strategy. It has also recently trimmed an overweight position in equities into its multi-asset absolute return and credit strategies.

Multi-factor investment inflows have exploded over the past decade. At the end of March 2018, there was $70bn (£51.9bn) in multi-factor investment, compared to just $3.8bn (£2.8bn) at the close of 2009, according to BlackRock.

A source from Haringey Council confirmed that the fund will follow this trend later in 2018, moving 42.6 per cent of its equity allocation to a multi-factor index.

Equities make up 45 per cent of Haringey’s portfolio. After the move, the fund will have 9.6 per cent allocations to both the hedged and unhedged RAFI Multi-Factor Indexes, managed by Legal & General Investment Management.

A multi-factor approach will diversify away from specific biases coming from any one factor

Grace Lavelle, P-Solve

In a report from a committee meeting that took place on March 20 2018, the fund recognised that “the equity portfolio is the most volatile section of the investment portfolio overall”.

In an attempt to reduce this risk, Haringey has thus rebalanced 75 per cent of its overweight equity position.

Two thirds of the redeemed funds will go to an existing multi-asset absolute return mandate, managed by Ruffer within the London Collective Investment Vehicle.

The remaining cash has been invested in its multi-asset credit mandate, which is managed by CQS. The scheme retains a slight overweight position in equities.

Multi-factor investing can reduce factor bias

Multi-factor investing involves combining the different characteristics that act as drivers of returns from securities, such as value, momentum, quality and low volatility.

The £1.4bn Haringey fund’s equity portfolio is currently entirely invested in market cap index-linked funds.

“One of the downsides of investment in market cap indices is that the fund is increasingly exposed to the largest and most expensive companies in each index,” it observed in its March report.

“This strategy is unlikely to perform well if we enter a period of equity market decline,” the committee wrote, adding that “in this scenario, the fund could actually suffer disproportionate losses”.

Incorporating multiple factors reduces the volatility associated with opting for a single factor, according to Grace Lavelle, a senior investment associate at consultancy P-Solve.

“A multi-factor approach will diversify away from specific biases coming from any one factor”, she said. Multi-factor investing also offers schemes a way out of market cap biases, she added.

The scheme’s equity strategy currently has fixed allocations to specific regions. The committee recognised that this restricts the flexibility of the scheme’s equity investment and does not allow for “the fluctuating size of different geographies within the global economy”.

“This can be overcome by the use of a global index which automatically rebalances different geographic weightings,” the scheme said.

Ensure factors complement each other

As of December 31 2017, the fund’s equity portfolio was valued at £790.6m. The planned reallocation would see £336.8m moved into multi-factor investment in global equities.

Factor investing or smart beta is often viewed as a middle way between active and passive management, offering a more selective approach to investment than passive, without the higher fees associated with active.

Aniket Bhaduri, senior investment consultant at JLT Employee Benefits, said that this perception explains the rising popularity of the investment approach, adding that most opt for multi-factor: “There’s not much appetite in the investor community to invest in single factor smart beta indices.”

He argued for an integrated multi-factor approach that avoids cancelling out the benefits brought by different factors.

Multi-assets help dampen volatility

As the scheme looks to integrate different investment factors and access more regions at greater speed, it has already taken steps to control the risk within its growth portfolio, diversifying its overweight equities.

Haringey seeks yearly returns of 8 per cent from its multi-asset absolute return strategy.

According to consultancy Spence Johnson, the UK pensions market has historically led the way in the volume of institutional multi-asset activity conducted in Europe, followed by Switzerland.

At the second quarter of 2017, the UK had more than €150bn (£131.1bn) in institutional multi-asset funds.

Scott Edmunds, investment consultant at Quantum Advisory, said that diversified growth managers, which participate in a significant chunk of multi-asset activity had become “the darling of the pensions industry” in recent years.

Under normal market conditions, Edmunds says, the asset class offers “reasonable return at dampened volatility”.

He is curious to see how it would deliver under stressed market conditions. “I think it would be quite interesting to see how these funds perform then and whether they do actually dampen down volatility,” he said.

Deon Dreyer, managing director at technology provider Ortec Finance, has witnessed similar activity at other schemes, as “investment consultants have become more sophisticated” in their methods.

Schemes such as Haringey can navigate the threat of equity risk “by either working on the equity side, or translating that into different asset classes which have similar overall return… and in addition, possibly have some diversification benefits”, he said.

MAC offers agility across markets

For its MAC mandate, another beneficiary of the rebalancing, Haringey targets returns of 5 per cent per annum against a benchmark of the three-month British pound sterling Libor interest rate.

Mike McEachern, portfolio manager and head of public markets at fixed income asset manager Muzinich & Co, thinks that the scheme’s commitment to MAC will offer the geographical flexibility it seeks, and will help it to reduce its investment risk.

“The ability to tactically move in and out of markets at select moments means an investor can capture opportunities and avoid challenges within each sub-asset class, region or ratings band,” he said.

“As each credit segment and region has different characteristics, the ability to reallocate depending on market conditions can also reduce volatility,” he added.

McEachern viewed the combination of a multi-asset approach to credit investing with an absolute return objective as an effective means to generate attractive returns across the credit cycle.

Under a stressed scenario, he underlined the importance of being able to make rapid tactical portfolio adjustments “free from benchmark constraints”, as well as the ability to use derivatives to manage interim market volatility.

Scheme retains low-carbon exposure

Haringey has also kept its faith in low-carbon equities. Following a review by Mercer in the summer of 2017, it upped its exposure from a third to half of its developed equities allocation, or 19.2 per cent of the overall portfolio.

In March, it decided to retain this allocation and opted to hedge out currency risk on the investment. The council declined to comment on this decision.

Equities have not been the scheme’s sole area of focus when it comes to environmental, social and governance issues. Last year, it invested £70m in renewable energy infrastructure, which amounts to roughly 5 per cent of the scheme’s investments.

Investing in low-carbon equities represents another way for the scheme to generate returns while reducing risk. Analysis by Credit Suisse in 2015 suggested that average annual returns from the coal sector could fall between 26 per cent and 138 per cent before 2025.

The scheme’s latest investment strategy statement reads: “The fund believes that further reduction in exposure to fossil fuel industries will reduce risk and secure stronger returns for the fund over the long term.”

Reuters adds MAC fund as trend expected to continue

The Reuters Pension Fund has invested in a second multi-asset credit fund and dropped a loans fund, as the lure of high risk-adjusted returns continues to draw investors to MAC products.

Kate Brett, principal of responsible investment at Mercer, said that while low-carbon equities are moving up the agenda of institutional investors, different regions are adopting different approaches to greener stocks.

UK investors take on a “broad market exposure”, according to Brett, while those on the continent prefer a “best in class” strategy.

“The tracking error between a low-carbon approach and standard approach is typically between 30 to 50 basis points, so you’re not taking on a lot of investment risk on that side,” she said.