Fujifilm is overhauling its defined contribution default fund to improve its performance and relevance to members, as schemes continue to rethink DC glide paths following the pension freedoms.

The introduction last year of additional choices for members at retirement has led trustees to look again at the suitability of their schemes' investment strategies, in particular the derisking phase leading up to retirement which has largely targeted traditional annuities only.

Managing Fujifilm's hybrid scheme

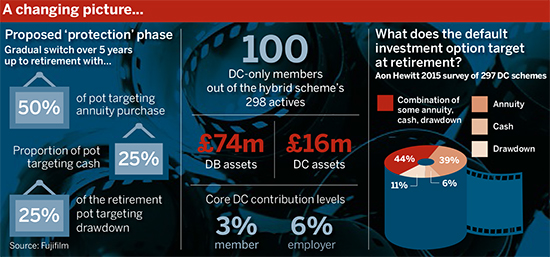

Fujifilm has a hybrid scheme containing a defined benefit section, which is now closed to new members, and a DC section. As at September 30 2015, the hybrid scheme had 298 active members, 418 deferreds and 113 pensioners – of the active members, around 100 are DC only.

It moved to a hybrid structure of core DB plus an optional DC top-up tier in January 2005, and then fully DC from March 2010. Active members with a DB pension retain final salary linkage for their pension accrued up to March 31 2010.

Satchell said the £74m DB section has performed broadly in line with the benchmark over the past two years, producing good nominal returns, particularly in 2014, although performance has been negative over the past six months.

He said: "The LDI strategy has proved successful, providing the expected protection to the funding level. The trustees are currently happy with the DGF performance since inception in 2013, having seen good equity-type returns but with less volatility."

Fujifilm is looking to proceed with a pensioner buy-in deal later in 2016.

The photographic and imaging company has a hybrid scheme (see sidebar) containing a defined benefit section, which is now closed to new members, and a DC section.

Fujifilm’s current growth phase runs to 10 years from retirement and is invested in global equities, while the “protection” phase gradually switches to produce 75 per cent in index-linked gilts and 25 per cent cash at retirement.

David Satchell, chair of trustees, said the scheme has tabled a revised structure to address two issues.

“Discussion started in 2014, the main concern being that a one-size-fits-all-default was no longer appropriate,” he said. “There was also concern about the performance of gilt and bond funds. The introduction of pension freedoms highlighted the need for change and accelerated our discussions as the old approach was clearly no longer relevant.”

Capturing growth

The proposed new structure will incorporate target date funds and feature a longer growth phase running up to five years from members’ assumed retirement date. The passive global equities will be replaced with diversified growth funds.

The lifestyling phase will target 50 per cent annuity purchase, 25 per cent cash and 25 per cent drawdown.

Members outside of the default have nine self-select funds to choose from, which the scheme is looking to increase to 11 funds including DGFs.

On DGFs, Satchell said: “The reduced volatility, whilst still benefiting from equity-like returns – which the trustees have witnessed in the DB section – is an important consideration and facilitates a shorter period over which funds are switched to the protection phase.”

Fujifilm is not planning to introduce an in-scheme drawdown facility but will keep the matter under review, paying particular attention to the overall appetite for drawdown from members.

Satchell added: “As trustees, we are embracing practical and existing solutions in order to address the issues facing us, rather than trying to break new ground. As a small-to-medium-sized scheme, we face the same issues as the very large schemes but believe that our strategy is both practical and effective for our size.”

The bigger picture

Nico Aspinall, senior investment consultant at Willis Towers Watson, has seen schemes move away from gilts and bonds during the lifestyling phase in favour of a low-risk multi-asset approach.

“In the situation where you don’t know what members want, it makes sense not to lock them into low-returning assets for a long period of time – bonds and gilts, but also cash,” he said.

We are embracing practical and existing solutions in order to address the issues facing us, rather than trying to break new ground

David Satchell, Fujifilm

Concern around the future performance of equities could make moving to DGFs now a good thing in terms of protecting against volatile markets, Aspinall said. But he added: “We have some concerns around their value for money relative to simpler approaches… There is a big range of approaches and levels of skill in the sector so it does matter which one schemes choose.”

Mark Futcher, partner at consultancy Barnett Waddingham, agreed and said it is important to be clear on the mandate of any given DGF and whether this fits the wider structure of the scheme, including how members are likely to use their pot at retirement.

But he voiced concern that many schemes are still basing their investment strategies on a one-off retirement date.

“It is clear that people are no longer accessing their pots at a single date and instead, for example, taking some cash at 55, topping up state pension at state pension age with an annuity and leaving the rest as a rainy-day fund in drawdown,” he said.

“The reality of how people are taking their pots means that most investment structures that target a single point are not fit for purpose.”