The Financial Conduct Authority has published its final rules requiring firms to provide an information prompt to consumers to improve shopping around in the annuity market, setting out a number of changes including an enhanced annuity warning.

The reliance on information and communications alone, especially in a market where people haven’t really engaged with their pension saving, will just lead to poorer outcomes

Darren Philp, the People's Pension

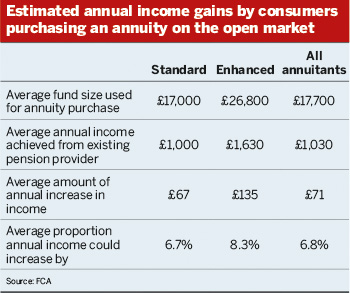

Behavioural research conducted by the FCA shows that when consumers are shown the annual increase in income that they could gain from purchasing on the open market, 40 per cent of participants went on to compare products from different providers.

The policy statement comes following the FCA's consultation on implementing information prompts to increase shopping around in the annuity market.

Enhanced annuities as an 'afterthought'

The statement, which was published on May 26, sets out a number of changes in response to feedback on the consultation, including the requirement for “the inclusion of a clear and prominent warning about enhanced annuities”.

Furthermore, firms engaging with consumers over the telephone will only have to provide the information prompt in relation to the specific guaranteed quote that a consumer has said they would like to proceed with.

The regulator has also changed the implementation date to March 2018 due to many firms commenting that the original September 2017 deadline was too challenging.

Most respondents to the FCA’s original consultation said that the regulator’s proposed approach did not make it clear that income could be enhanced for consumers with medical conditions or if certain factors relating to the consumer’s lifestyle were applicable.

Nathan Long, senior pension analyst at platform provider Hargreaves Lansdown, noted that the FCA has now “realised that it needed to include enhanced annuities” in the information prompt. However, he said that it seems to be “bolted on” as an afterthought, meaning that “it doesn’t really encourage people who have health issues to shop around quite as much as it should do”.

It is relatively common for someone of retirement age to be taking medication for high blood pressure or high cholesterol, factors that may contribute towards someone being able to qualify for an enchanced annuity, said Long.

“So for it to be tagged on as a ‘did you know?’ might limit its effectiveness," he added.

Comparisons

FCA research conducted in 2014 found that, of all the consumers that chose to remain with their existing product provider and purchase an annuity, 80 per cent of those people would have got a better deal had they shopped around the market.

Stephen Lowe, director at specialist financial services company Just Group, said that, in the FCA's conclusion, “the basis for how the [annuity provider] comparison is done, has not taken into account that fantastic insight...that shows that 8 out of 10 people get a better deal by moving on, predominantly driven by the need to collect additional information around medical [details] and lifestyle”.

Lowe explained that some companies only use date of birth and amount the consumer has to invest in order to generate an annuity price. Therefore the comparison a consumer does in the market only has to ask those two questions of every other provider.

A different company may use a fully individually underwritten set of questions, and that basis of comparison takes all of those questions and compares against all the other providers in the market, he said.

Consequently, customers “could believe they’re getting a whole of market comparative piece of information, when they’re not”, he added.

Additional information may not help

While the FCA has said that it will put a risk warning on the information prompt that says consumers may be able to get a better deal by getting an enhanced annuity, Lowe said that information prompts may not be enough.

“The FCA’s remedy is only a partial solution at best,” said Darren Philp, director of policy and market engagement at mastertrust the People's Pension.

He also cited the FCA’s research that showed that 80 per cent of people lose out by purchasing from their own pension provider.

He also said, while the FCA’s solution will help some people benefit from an information prompt, it is not enough to help those consumers who would benefit from switching provider.

“Consumers find shopping around for an annuity very very difficult – quite often they don’t know the type of product that they actually want, and people quite often misunderstand what an actual annuity is,” he said.

Providing people with more information is not enough. “The reliance on information and communications alone, especially in a market where people haven’t really engaged with their pension saving, will just lead to poorer outcomes,” stressed Philp.

He suggested that the provider could "have a fiduciary duty or a legal responsibility not to put them in a worse performing product. That would shake up the market and ensure that consumers get the best deals”.

Similarly, Jon Dean, senior consultant at Altus Consulting, said that “I’m not convinced adding a warning about enhanced annuities will increase shopping around”.

While “telling a client they have been sent a market-leading quote but they can still get more income could be confusing. However, it may prove impractical to fully underwrite all annuity quotes, so I understand why the FCA has taken this stance,” he added.