The Specialist: Advice and guidance are stand-out concerns as drawdown strategies proliferate following freedom and choice.

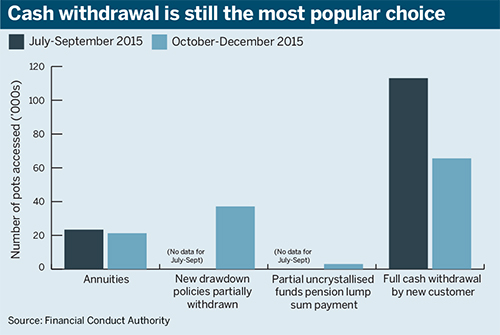

Data from the Financial Conduct Authority show that in the quarter from July to September 2015, of the 178,990 pensions that were accessed, 30 per cent used both partial and full income drawdown, 23 per cent of which were full withdrawals using small pot lump sum payments. This compares with only 13 per cent of new retirees who chose to purchase an annuity.

People are still interested in buying annuities, but they’re perceived by many as not offering great value, and the providers offering them are not trusted by some people

Alice Evans, Willis Towers Watson

The freedom and choice reforms introduced in April 2015, which gave pension savers the option not to annuitise, have brought a very different, more diverse, demographic of customers to the market looking for alternatives to the old way of buying income in the form of an annuity.

“Obviously annuities are still around. People are still interested in buying annuities, but they’re perceived by many as not offering great value, and the providers offering them are not trusted by some people,” says Alice Evans, head of commercial and client development at consultancy Willis Towers Watson.

“Annuities require people to make an irrevocable decision to hand over all their savings in exchange for a regular income – which is something many are hesitant about doing whilst they are still thinking through their retirement plans,” she says.

Although annuities are still around, industry experts believe that the poor take-up is due to people’s general assumption that they are poor value.

Jamie Jenkins, head of pensions strategy at insurer Standard Life, says there is evidence of people looking at different drawdown options for their pension pots after withdrawing the initial lump sum of tax-free cash. He says the decision to buy an annuity becomes more relevant in later life when pensioners feel their income needs are becoming more stable.

“Actually, buying an annuity [in] later life for many people might be a good way of doing it rather than trying to commit to a particular shape of income at age 60,” he says.

According to FCA data, 120,969 pensions were fully cashed out over the July to September period following the pensions reform, and 88 per cent of these were for customers with small pots below £30,000.

The data are in line with industry experts’ observations.

“With £30k or less an individual member might not be able to move into a post-retirement solution, so you do see some issues of access with smaller pension pots,” Stephen Budge, principal in Mercer’s UK defined contribution and financial wellness team, says.

“This has a lot to do with many providers having a minimum criteria of accessing drawdown, which can be between £30k and £50k after taking tax-free cash,” says James Haggon, consultant at LCP, pointing out that many retirees are currently enrolled in a defined benefit scheme, which means that money in a DC scheme “might just be a little bit of extra and they might take it out as cash”.

In-scheme drawdown

Some pension schemes have opted to set up their own drawdown solutions; for example, Thomson Reuters introduced in-scheme drawdown last year.

However, although different types of drawdown solutions are increasing in popularity, the uptake of in-scheme drawdown solutions has not been high. Haggon says this is due to the extra governance issues and complex regulation around default funds.

“It puts a lot more pressure on the trustees who would have responsibility for a completely new population of pensioners; a very different kind of population with different needs than the trustees are used to. And these needs would linger on for quite a long time,” Haggon says.

He also points out that in terms of investment, trustees need to make sure that there are suitable options available for a default fund for members who wish to access drawdown. This could be a daunting task, as the investment methods used in decumulation differ from those in the accumulation phase.

“It’s targeting growth whilst also aiming to protect the current fund,” Haggon explains.

Choosing the right strategy is crucial for a successful drawdown phase. Which strategy is right for a individual depends on a number of factors, such as whether they want to draw income from the pension capital, draw only the income generated by the investments themselves, or simply leave the pension pot to grow after taking the tax-free cash.

Investment choices vary from very conservative, which allocates between 80 per cent and 90 per cent to low-risk investments such as corporate bonds, to very aggressive, which allocates closer to 90 per cent to shares, keeping the remaining 5 per cent to 10 per cent in bonds.

Diversification is one of the keys to reducing risk in the portfolio, and it can be useful to keep a cash buffer, which will enable the investor to still draw income should the market fall.

The expected yields can vary, mostly between 3 per cent and 5 per cent. However, the different drawdown strategies have not evolved significantly during the year. According to Budge, this is due to the suppliers being more concerned about product development.

He says the investment choices and sophistication of the investments “haven’t necessarily been the first step”.

Despite this, he says their development might start to play a more important role in the future.

Looking ahead

So what is currently available for people who do not want to annuitise but opt for a drawdown arrangement in a market still very much dominated by retail-type solutions such as self-invested personal pensions? And how is guidance and advice organised around these options?

“It very much, unfortunately, depends on the type of arrangement you’re in, the provider you’re with and whether you’re lucky enough to be in one where they have developed their proposition to meet your specific needs,” Budge says.

However, he emphasises that things are evolving very quickly: “One will have focused on developing one thing and another may have taken another approach. Eventually there will be a very comprehensive range of options on offer, I’m sure.”

Jenkins says that emphasis on advice and guidance is key in developing a successful product that improves client outcomes.

“I don’t think the market needs a lot of innovation; there are a good number of choices already available on the market in terms of the various things people might want to do. People can already mix and match products, annuity and drawdown, to suit their income needs,” he says.

“The real area of development is around advice and guidance and how to bring that forward; engaging with people earlier.”

Budge agrees: “Any post-retirement solution has to be combined with some form of governance, member communication, guidance and access to advice. The package is really the key to any successful product in that space.”

The rise of mastertrusts

Recently the market has seen an increase in so-called mastertrusts. They are not retail solutions, but are available for schemes that want to partner with drawdown providers. They are cheaper than retail products such as SIPPs, and many are designed around self-service, giving people tools and information to help them make their own decisions.

Trustees will use mastertrusts to deliver the post-retirement freedoms for people who leave employment, and it will be from there where they can access the flexibility with their savings

Stephen Budge, Mercer

Evans states that mastertrusts will play a significant role in the future of the decumulation market.

“The products that already exist will change and adapt to this wider, more diverse demographic. And it will take time for providers to do that. But there are new approaches out there, many emerging from the mastertrust space – which are focusing on a lower-cost, consumer-grade experience. That is where we see the market going,” she says.

Budge says proper through-retirement solutions will be of increasing significance in the post-retirement market.

“I think that is where the trend will be; sticking with existing trust-based arrangements. Trustees will use mastertrusts to deliver the post-retirement freedoms for people who leave employment, and it will be from there where they can access the flexibility with their savings,” he says.

Jenkins says: “It’s not that somebody should be a pensions expert or investment expert, they really needn’t be. But they have to know their plan, and what we’re trying to do is to create a solution to that plan.”

Janina Sibelius is a reporter at Financial Times publication MandateWire