Data crunch:Pensioners could miss out on an additional 6.7 per cent in retirement income if the government goes ahead with plans to downgrade the retail price index, an analysis has revealed.

Projections by Insight Investment and Pensions Expert show that a member of a defined benefit pension scheme who is retiring at age 65, on a starting income of £20,000, could lose £33,637 over the course of their retirement if the housing variation of the consumer price index is applied to their RPI promises, as chancellor Sajid Javid indicated last week.

With the UK Statistics Authority recommending the government scrap RPI, Mr Javid agreed to consult on whether to bring the methods in CPIH into RPI between 2025 to 2030, effectively aligning the measures before putting an end to RPI at some point in the future.

In a statement, the chancellor said this would address RPI’s shortcomings in the interim and “give users time to prepare for the many complex effects such a change will have”.

Is it fair to take £100bn from pension schemes just to make the statistic better?

Jos Vermeulen, Insight Investment

This means there would be no change to the measure before 2025, at the earliest.

From 2030, the requirement for the UK Statistics Authority to consult the chancellor before making changes to the coverage or calculation of the RPI falls away.

It is worth noting that a move from RPI to CPIH has no impact on defined contribution members, unless they buy an annuity or hold assets linked to those inflation measures.

CPIH is usually held to be a more accurate measure of inflation, but what would be the impact on DB pension scheme member benefits?

Rule change transfers wealth from pensioners to government

An RPI-linked pension worth £505,292 with a 1.5 per cent discount rate would be knocked down to £471,655 under CPIH, meaning the overall present value of their pension would be reduced by 6.7 per cent in real terms.

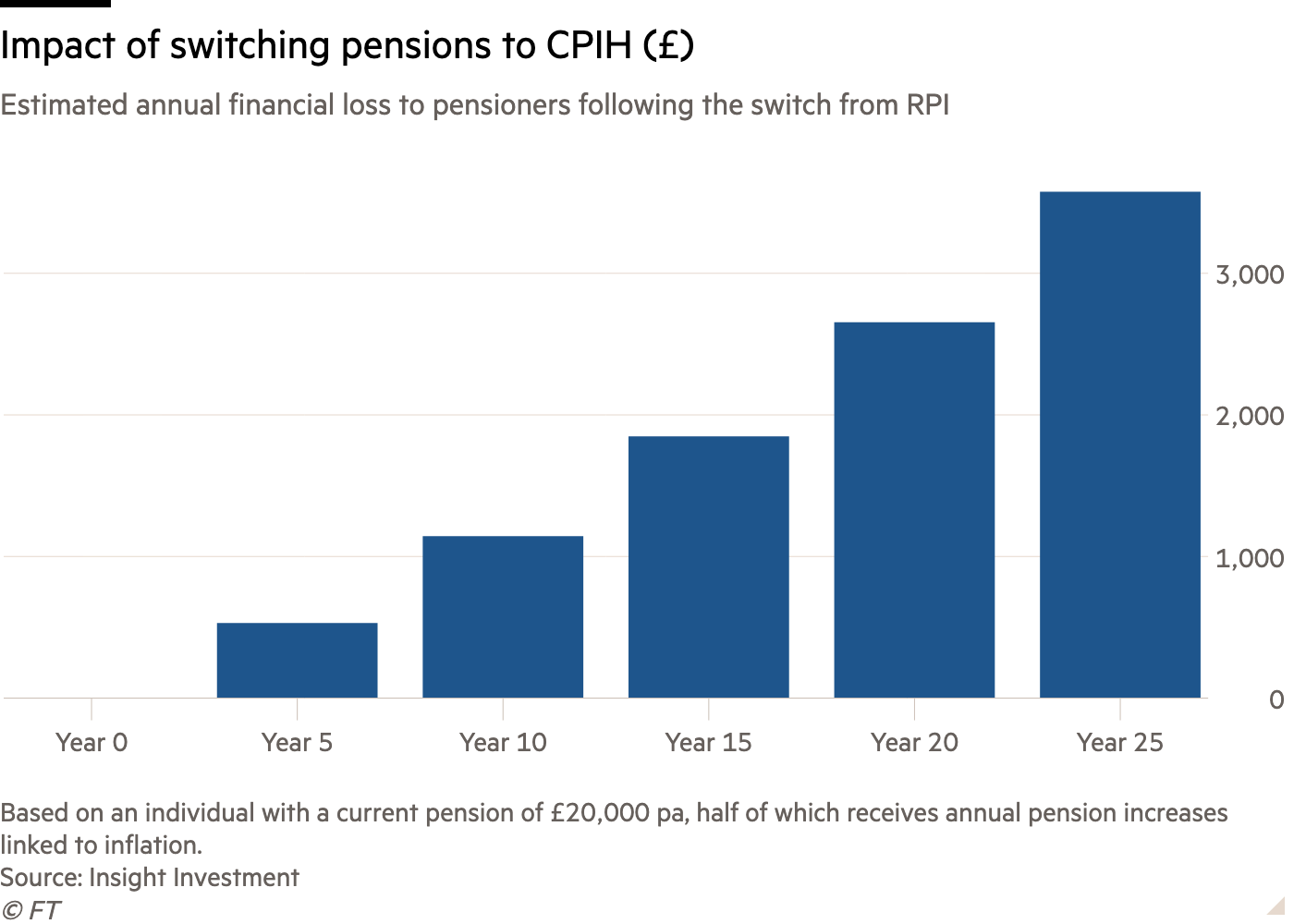

The chart below shows how the proposed change to pension increases could tangibly reduce many pensioners’ future incomes.

The calculations were based on an individual with a life expectancy of 24 years at retirement, and half of their pension received annual pension increases linked to inflation.

It assumes RPI at 3.5 per cent, and CPIH at 2.5 per cent a year. The Office for National Statistics’ favoured CPIH is roughly 1 percentage point lower every year than the RPI, which is the assumption that has been used.

Should members be compensated?

According to Jos Vermeulen, head of solution design at Insight Investment, if RPI must be changed it is very important that pensioners are compensated.

He explained: “The best outcome for plan members would be for RPI to remain untouched... we understand the statistical arguments about RPI and the desire for good inflation statistics, but that is a debate which should not cause transfers of wealth from one group to another.

“If RPI is changed, then its redistributive effects need to be offset. If the changes just went ahead as suggested – by which in 2030 RPI becomes CPIH in another name – then the government will have cut its debt by more than £100bn, taken from the holders of index-linked gilts.

“Those holders are predominately UK pension schemes, who in turn will pay pensioners lower pensions. Is it fair to take £100bn from pension schemes just to make the statistic better?”

Mr Vermeulen added: “In all likelihood, the 2020 consultation will be the industry’s last chance to ensure the government adequately compensates the holders of index-linked gilts and to ensure that pensioners’ future incomes are protected.”

Government signals end to RPI

The end may be nigh for the flawed retail price index of inflation, after the chancellor announced plans to consult on whether to align it with a version of the consumer price index between 2025 and 2030. Read more

Also commenting on the figures, Tom Selby, senior analyst at AJ Bell, said: “I think this reinforces the fact the shift away from RPI, whenever it happens, will be messy and the government and the ONS will need to consider the impact on the existing stock of products and benefits.

“I suspect the ONS will need to keep producing a notional RPI for a number of decades to ensure these contracts are honoured.”

Mr Selby added: “One would also assume new arrangements linking to RPI will need to be phased out if the inflation measure is eventually ditched.”