Debenhams pension scheme trustees have secured higher employer contributions as part of the recovery plan despite having reached an IAS 19 surplus earlier this year, demonstrating the discrepancies between two scheme funding calculation methodologies.

Many sponsors of defined benefit schemes have been forced to increase their contributions to combat the effect of low interest rates, even as the Pensions Regulator’s 2014 DB funding code encourages schemes to take into account the financial strength of the employer when negotiating higher contributions.

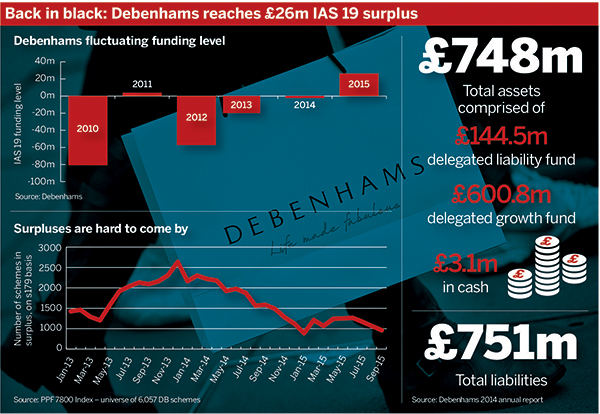

The department store’s £748m pension scheme reached an IAS 19 surplus of £26.2m as of August 29 this year, up from a deficit of £2.4m in 2014. The company attributed this to better asset returns, in particular the liability-hedging component.

In its full-year results, released last week, the group said: “During June 2015, the triennial actuarial valuation was completed and a new agreement was concluded under which the group agreed to contribute £9.5m per annum to the pension schemes (previously £8.9m per annum) for the period from 1 April 2014 to 31 March 2022, increasing by the percentage increase in RPI over the year to the previous December.”

The company also covers non-investment expenses and levies, including the Pension Protection Fund levy.

Differing calculations

Hugh Nolan, chief actuary at consultancy JLT Employee Benefits, explained that the IAS 19 or accounting deficit, and the actuarial valuation funding estimate were calculated using different methodologies.

He said: “The accounting basis is meant to be a best estimate and the funding basis is meant to be prudent… The best estimate we use is based on a notional investment in corporate bonds, whereas the funding basis is based on what the trustees are actually doing.”

It illustrates the difference between the frankly notional figures that exist in company accounts and the hard reality of cash

Alan Collins, Spence & Partners

Nolan added: “Once you take account of the real investment strategy and put some prudence in there you can get quite different values… I see all the time other schemes where the actual investment strategy they’re using is very different from the IAS 19 basis.”

Alan Collins, director at actuarial consultancy Spence & Partners, said the actuarial valuation could be a shock to employers whose schemes were seemingly well-funded on an IAS 19 basis.

He said: “When you’ve got big schemes and reasonably well-funded schemes, the pounds-and-pence difference between [accounting level] and funding can look enormous.”

He added: “It illustrates the difference between the frankly notional figures that exist in company accounts and the hard reality of cash.”

Trapped surpluses

Defined benefit scheme trustees must pass a resolution ahead of April 2016 if they wish to retain their current power to repay surpluses to their employer sponsors.

While pension scheme surpluses appear out of reach for many UK DB schemes, trustees of well-funded schemes will lose the ability to refund surpluses in ongoing arrangements if they fail to pass what is known as a section 251 resolution before April 5 next year.

Investing for income

DB funding can be a significant burden for employers and many are exploring ways to manage the risk cost-effectively. Last week, consultancy Hymans Robertson released its FTSE 350 report, which looked at the 217 companies on the index with DB schemes “material” enough to be disclosed under IAS 19.

The report found that while 50 per cent of the companies were cash flow negative, or soon would be, only 4 per cent saw investing for income as a priority.

Jon Hatchett, partner at Hymans, said companies had paid £250bn into their schemes since 2000, but “the deficits are still there”. He said: “Schemes haven’t built in resilience to risk.”

Hatchett advocated longer-term funding plans with lower annual contributions as a way to minimise the cost to employers without sacrificing results.

“In most cases schemes tend to be rushing to get fully funded,” he said. “Less risk and less cash, but paying the cash for longer… can be attractive to the company.”