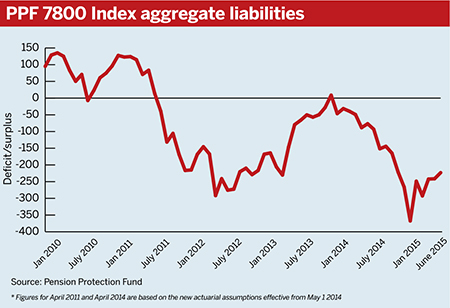

Data analysis: Defined benefit schemes’ aggregate funding ratio rose slightly to 84.8 per cent in June, according to data, but experts say schemes should further hedge liabilities to buffer against underlying volatility in the bond markets.

The monthly figures from the Pension Protection Fund 7800 Index also showed a slight decrease in the deficit of the 6,057 schemes measured, to £223.1bn in June from £241.3bn at the end of May.

However, some industry commentators have noted the figures belie a more complex environment in which the focus of scheme funding volatility has moved from asset prices to liabilities, as a result of movements in government bond markets.

PPF 7800 Index key stats

The aggregate deficit decreased over the month to £223.1bn from £241.3bn at the end of May (but up from £76.8bn in June 2014).

The funding ratio increased to 84.8 per cent from 84.1 per cent over the month (compared with 93.8 per cent in June 2014).

Total assets were £1.24tn and total liabilities £1.47tn.

Of the 6,057 in the index, 4,794 were in deficit and 1,263 schemes in surplus.

Daniel Peters, partner at consultancy Aon Hewitt, said that in this environment hedging liabilities is more important than ever.

“A well run LDI portfolio can provide excellent protection against the vicissitudes of bond markets,” he said.

“Equally important at the current time is diversifying exposure to risk assets, rather than relying on the equity market bet to continue to come through.”

Simeon Willis, chief investment consultant at KPMG, said the PPF index is based on a “relatively simplistic” estimate of asset returns and ignores derivative overlays such as liability-driven investment hedges.

“Therefore, in an environment where volatile yield movements are driving funding level changes, the index may overstate the extent to which funding levels are actually moving,” he said.

“For instance the relatively modest improvement over the last month appears to be driven by falling liabilities – which in actuality are also likely to have been reflected in asset side movements where the liabilities are hedged, which would have dampened the impact.”

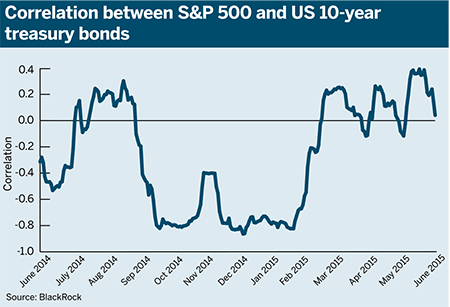

The graph from asset manager BlackRock shows an increasing correlation between equities and bonds over the first half of this year, which could heighten schemes’ overall risk exposure.

Willis added that the factor keeping long-term yields low will not disappear over the short-to-medium term, and as such the “obvious choice” would be to remove as much interest rate and inflation risk as possible.

Risk agnostic

However, Tom Brooke-Smith, senior investment consultant at Towers Watson, said “no one risk should dominate” schemes’ approach to risk management.

Low returns from risky assets and a “slow path” to interest rate reversion mean schemes should consider whether current portfolios are suited to the future investment environment.

Brooke-Smith said: “It is crucial that investors decide to either ride out a period of low returns, or to reduce risk in expectation of improved returns in the future.

“Riding out requires a necessarily long-time horizon, while reducing risk is consistent with an expectation that downside outcomes are real and prevalent.”He added that the current bond market environment means reducing inflation and interest rate risk is attractively priced.