EMD survey: While reports abound of big-name emerging market specialists taking a severe hit in the summer sell-off, investors elsewhere are asking themselves how they can capitalise on the hysteria.

In the case of emerging market debt, the in-roads are steeped with hazards and unknowns, but many investors such as pension funds are trying to find ways to negotiate the complexities to access diversification and higher yields.

One such investor is the £535m government-backed mastertrust Nest, which earlier this month detailed plans to tender for an EMD mandate. Its chief investment officer Mark Fawcett is all too aware that the asset class carries risk, but it is EMD’s risk profile in particular that he hopes will act as a diversifier to the scheme’s EM equity exposure.

Emerging bond markets have deepened substantially and the investment opportunity there is only set to grow

Lucinda Downing, Aon Hewitt

Asserting the long-term credentials of the asset class, Fawcett says: “Emerging market debt is riskier than investing in gilts or US treasuries. That’s why we’ve gone down an active route, because it needs to be managed carefully.”

But while the virtues of EMD from a long-term perspective may be many, getting the entry point right is still important for pension funds and with such a nuanced asset class, through which door you enter becomes critical.

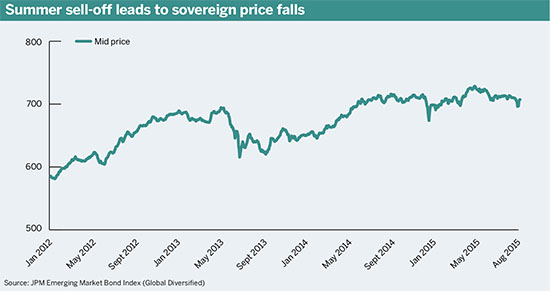

Is the party over?

Lucinda Downing, multi-asset manager in consultancy Aon Hewitt’s global asset allocation team, says there are good “pockets of value” to be found in the asset class, alongside parts of the market that are “cheap for a reason”.

She adds: “It is very easy to be too downbeat about emerging market prospects. We expect emerging economies to recover over the medium-term, driven by improved global growth and increasing demand from the growing middle class. Emerging bond markets have deepened substantially and the investment opportunity there is only set to grow.”

Commentators have been keen to emphasise the heterogeneity within EMD, the idea that the asset class is in fact several asset classes, which include currency, sovereign and corporate debt, overlaid with the idiosyncrasies of the investee countries.

Chris Redmond, head of manager research, fixed income, at consultancy Towers Watson, says this provides a range of different risk-return characteristics for schemes to consider, adding: “An interesting question going forward is whether or not hard currency sovereign emerging market debt will deliver the same risk profile as we enter the next phase of the interest rate cycle in developed markets.”

There are four major themes driving hard currency sovereign credit spreads: commodity dependence; external vulnerability; exposure to a slowing Chinese economy; impact of US dollar strength.

There are four major themes driving hard currency sovereign credit spreads: commodity dependence; external vulnerability; exposure to a slowing Chinese economy; impact of US dollar strength.

Redmond says: “Understanding how these four themes develop will be an important driver of where the opportunities will lie, in particular whether those sovereigns/corporates currently suffering stress provide a good entry point.”

Aside from timing, pension schemes need to consider whether their portfolio will be better suited to investments made in hard currency or local currency.

The relative battering that local currency-denominated debt received in the past couple of months will either repel investors or cause some to view it as a contrarian buying opportunity.

Pete Drewienkiewicz, head of manager research at consultancy Redington, says: “[If you] do not believe that developed market rate rises will hurt EM currencies – which it is easy to argue they will – then local debt undoubtedly looks appealing.”

However he adds that finding skilled, unconstrained managers in this field has been difficult.

“We recently performed a manager selection exercise within local debt and it is, however, fair to say that we were very disappointed with the quality of our meetings, once again reiterating our tendency to prefer less constrained, benchmark-agnostic mandates,” he says.

What exposure?

Consultants and asset managers we spoke to cast the expected returns as anywhere between 4 and 8 per cent, but emphasised the need to take a longer term position.

An interesting question going forward is whether or not hard currency sovereign emerging market debt will deliver the same risk profile as we enter the next phase of the interest rate cycle in developed markets

Chris Redmond, Towers Watson

Drewienkiewicz says any strategy a pension fund invests in should be a minimum 5 per cent to avoid over-diversification, but says he would not feel comfortable allocating much more than this to EMD unless the scheme had a particularly strong view on the asset class.

The type of mandate will depend on each scheme’s risk appetite but, importantly, their ability to find a suitable manager.

As well as risk tolerance, Redmond says other factors such as governance and desired return will also come into play when deciding how to gain EMD exposure.

“Speaking in fairly general terms,” he adds, “emerging market debt [is] under-represented in investor portfolios and failing to appropriately reflect the rich and broad opportunity set available.”

Redmond takes this one step further and says the more fluid mandates that remove what he calls the “arbitrary delineation” between emerging and developed markets have held up admirably throughout the recent volatility.

Aon’s Downing says EMD is one of the most under-invested asset classes by UK pension funds, and one which she feels warrants an equal strategic footing with other fixed income sectors within the return-focused portion of a fixed income portfolio.

Multi-asset credit, absolute return and total return have proved popular among Aon’s pension scheme clients, and Downing says they make sense for smaller schemes due to their diversification across bond sectors.

“However, we would advise that larger schemes should also consider direct investment in emerging market debt funds,” she says.

“Blended emerging market debt funds, which include local and dollar-denominated as well as sovereign and corporate debt, is a good first step into the area.”

Read part one of the EMD survey here, which looks at performance of the asset class