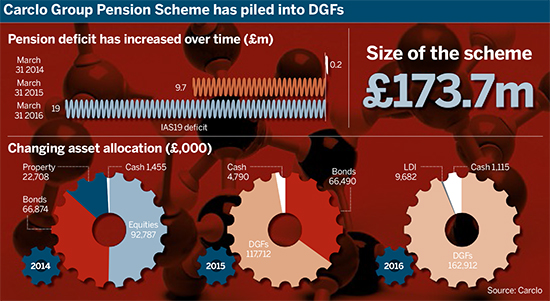

Technical plastics manufacturer Carclo is adding liability-driven investment mandates and continued support for diversified growth funds to its defined benefit scheme portfolio, after poor equity market performance saw its deficit almost double.

Carclo’s annual results, released earlier this month, showed a scheme deficit of £19m at March 31. The fund had a deficit of £9.7m the previous year, and was in surplus in 2014.

While its liabilities fell slightly over the past year, the scheme’s assets decreased by more than £15m, which reflected “the poor performance of equity markets during the year”, according to the group.

If you still need some good returns the alternative is active management, which is absolutely uncomfortable because large parts of the industry are pretty terrible at doing it

Matt Tickle, Barnett Waddingham

The £173.7m scheme has no direct equity holdings, instead allocating £162.9m to DGFs as of March. Despite the loss, the company said in its final results for the year: “The revised investment strategy of the scheme pension trustees to invest in diversified growth funds assisted the performance of the scheme assets relative to the broader performance of equities.”

A spokesperson for the company added in a statement: “The point of DGFs is that they allow a much more active investment choice [...] A well-managed DGF can therefore react quicker to equity falls.”

Performance anxiety

Many DGFs have underperformed recently according to experts, as diversification across asset classes proved not to be immune to market volatility.

“There have been products in the market that have had some drawdowns,” said Thomas Nehring, head of institutional and wholesale distribution UK and US at DGF provider Nordea. “It is a difficult thing to play macro, we’ve seen many examples of that.”

Instead of diversification across asset classes, Nehring advocated a more focused approach, separating several risk premiums, or risk/return drivers, from individual assets. “What you’ll see is these components actually act quite differently in different periods,” he said.

“It might be that we like the credit premium [of a bond] but we don’t like the duration premium, so what we’ll do is take on the credit premium and hedge out duration.”

Matt Tickle, partner at Barnett Waddingham, agreed that more “granular” approaches to DGF fund provision could benefit pension schemes.

But he said the overriding priority for funds would be to accurately assess the quality of DGF manager performance.

“Market returns are just increasingly difficult to get so therefore if you still need some good returns the alternative is active management, which is absolutely uncomfortable because large parts of the industry are pretty terrible at doing it,” he said.

Tickle said he expected DGFs’ popularity to steadily increase, with defined contribution schemes relying on them to reduce volatility for savers nearing retirement.

“It’s actually when you’re taking most equity risk, when you’re in your 50s,” he said. “So having a form of DGF or multi-asset type approach probably sits quite well.”

LDI provides vital protection

Carclo’s trustees agreed a revised funding strategy in 2015 in response to the growing deficit, combining “investment returns with affordable annual employer contributions”. The company contributed £1.1m to the scheme over the past year.

The scheme also allocated £9.7m to LDI strategies, a new addition to its portfolio.

The spokesperson said: “We have added interest rate and inflation hedges into the portfolio. The net result should be a reduction in volatility.”

Craig Gillespie, investment consultant at Aon Hewitt, said a lack of LDI implementation meant interest rate risk had hampered many schemes’ progress over the last three years.

“If you’ve hedged away that interest rate risk, the fact that gilt yields have fallen over that period, then it has been a lot easier for you to outperform just simply using equities,” he said.