The Alstom Pension Scheme has agreed an increase in recovery plan contributions following a drop in its funding level, but the decision has been buoyed by a strengthened sponsor guarantee.

Low yields from gilts and UK corporate bonds have dented the funding of many schemes, but a sponsor that is willing to provide guarantees can be a significant aid in adverse conditions.

Watch out the trustees don’t overcommit to a risky investment strategy

Hugh Nolan, Spence & Partners

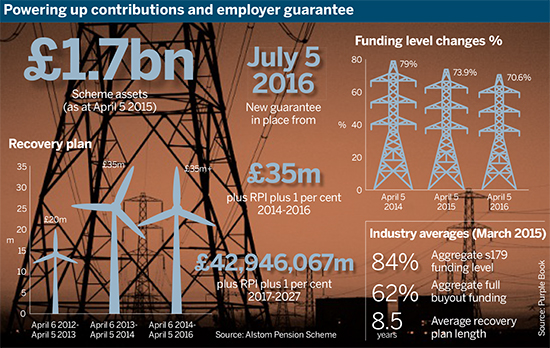

The most recent funding update showed that on April 6 this year the scheme had a funding level of 70.6 per cent, with a shortfall of £657.8m. This is down from 73.9 per cent on the same date last year and 79 per cent in 2014.

The fund said in a newsletter for members: “This reduction in the funding level since the valuation as at 5 April 2015 is mainly due to a slight fall in gilt yields which has increased the value put on liabilities and because the estimated return on the scheme’s assets was lower than expected.”

Extra company contributions

It added the factors mentioned had been partially offset by additional company contributions. The trustee and company agreed a revised funding plan, increasing the contributions agreed under a plan that started in 2012.

The previous plan paid a total of £20m between April 2012 and April 2013 in monthly instalments. This increased to £35m until April 2014. The contributions were then due to increase in line with the retail price index plus 1 per cent until 2027.

However, under the new plan, the contribution will be £42,946,067 from April 2017 and will rise in line with RPI plus 1 per cent afterwards.

Alstom Power, a UK arm of French multinational Alstom, was acquired by US conglomerate General Electric late last year, changing the sponsor of the Alstom Pension Scheme. GE group has now given the scheme a guarantee effective from July 5 this year.

The newsletter stated: “The guarantee is unlimited as to time and amount and improves the covenant supporting the scheme.”

It added that the guarantee has also allowed the trustee to scrap a “reduction factor” of 20 per cent that had applied to cash equivalent transfer values.

‘Sensible solution’

Lynda Whitney, partner at consultancy Aon Hewitt, said the guarantee sounded “like a very sensible solution”, but that “the trustees would need to look at it and make sure they have [security].”

She added: “Any principal employer of a pension scheme [is] on the hook for an unlimited time and amount, but you don’t usually see it written down like that.”

Where a scheme is attached to a subsidiary company, she said, often the scheme’s covenant will only apply to that subsidiary, leaving the scheme vulnerable should assets be moved around.

Watch out for break clauses

A strengthened covenant guarantee can be a boon for schemes, improving their flexibility to pursue higher investment returns.

However, Hugh Nolan, director at consultancy Spence & Partners and president of the Society of Pension Professionals, echoed Whitney’s view that trustees should investigate their guarantee thoroughly.

He said even with a guarantee, trustees should not consider the scheme to be completely secured.

HP scheme reboots parent company guarantee

The Hewlett-Packard Limited Retirement Benefits Plan has replaced its parent company guarantee following a major corporate reorganisation, resulting in improved terms for members.

“With any corporate structure you always have the possibility of a particular company being left without any assets; they just need to check the company giving the guarantee.”

He said it is important to “watch out… the trustees don’t overcommit to a risky investment strategy” as a result of the real or perceived security the guarantee gives.

Nolan added that guarantees often include break clauses that can be triggered in certain circumstances.

“I suspect there may be a facility for it to be withdrawn in the future,” he said.