Schemes are considering implementing currency hedges on risky assets as investment experts predict currency adjustments after a long period of relative stability in the developed world.

Experts have said as economies begin to grow and central banks reduce quantitative easing it is more likely that exchange rates will become more volatile, impacting schemes’ assets in foreign denominations.

Case Study: National Grid

In March, the £15.5bn National Grid UK Pension Scheme, through its in-house manager Aerion Fund Management, implemented a £3.5bn active currency overlay mandate for its overseas assets with asset manager Berenberg.

Paul Sharman, CEO of Aerion, said in a statement that the scheme was looking for ways to enhance the investment returns for members of the scheme.

“By actively managing the currency exposure of our overseas assets we are able to both limit the risks and maximise the potential of holding investments not priced in sterling,” he added.

A spokesperson for National Grid said: "It was implemented in order to manage the currency exposure in the asset portfolio and maximise currency hedging opportunities."

This has led some schemes, such as the National Grid UK Pension Scheme, to implement currency hedging to mitigate the risk of fluctuations (see box).

Malcolm Leigh, senior manager research consultant at Mercer, said there has been more interest in currency hedging than in the recent past. “I would have thought that with currency movement will come increased interest from schemes of all kinds, including UK schemes,” he added.

The reason for this interest has come from the period of relative stability in euro, dollar and sterling exchange rates. “When that happens for an extended period of time, an adjustment is more likely than it was in the past, and is more likely to be large than it was in the past,” Leigh said.

There is anticipation that as developed economies see renewed growth, those adjustments may take place. “So now is a good time to get prepared against that eventuality,” he said.

James Kwok, head of currency management at asset manager Amundi, said interest in currency hedging is expected to rise as a large portion of UK pensions’ overseas equity exposure is to US markets.

Over the past few years, hedging was less attractive to schemes as the US and British economies were performing fairly similarly. “There is more of a chance the sterling will outperform – it makes sense to hedge back into sterling,” he said.

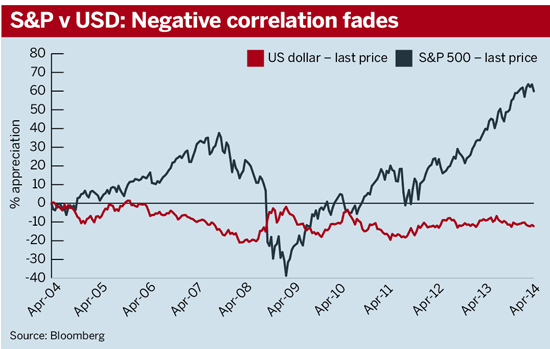

Another key factor that may lead schemes into hedging is the dissipating negative correlation between the US dollar and US equity market (see graph). This had meant schemes’ portfolios were less volatile if they owned both assets.

“Now that the negative correlation is diminishing, it is time for the UK pension investor to think about whether it is good to hedge back more foreign assets in sterling,” Kwok said.

Schemes are also looking to hedge the Swiss franc and the yen. Many have not hedged their emerging market currencies as appreciation was expected. However, EM currencies did not perform well last year.

“On a long-term horizon, a lot of EM currency have not moved since 2007; they have had a lot of volatility but didn’t really move,” Kwok said.

Scrutinising trades

Nick Spencer, director of alternatives at Russell Investment, said schemes are continuing to scrutinise the risks they are taking.

“We have been engaged in actually looking at the effectiveness of the FX trades,” he said. “A lot has gone to the custodian… but pricing in the custodians is not clear and there is not exactly the same attention to the best price.”

Russell has done work with local authority schemes to employ independent traders to buy and sell currency, rather than leaving the function with custodians, which can reduce costs from an average of 9 basis points to 1 or 2bp, he added.