The latest news and goings on from the PLSA’s annual investment conference in Edinburgh

Day 3: Thursday 8 June

3.20pm

We’re on the final straight, so hello from the auditorium for the session titled Economy and Pensions — The Challenges for a New Government… yes it’s the penultimate session of the conference with Ed Balls, strictly star extraordinaire.

This is Ed’s third visit to the PLSA investment conference, the first being in 2007 as AE was just making its way onto the agenda. He talks through the three ‘once in a lifetime’ events that have played out since his first visit: the global financial crisis, the pandemic and now war on the continent of Europe.The cumulation of those events has made planning for long term stability, which is fundamental for pensions, particularly difficult.

He talks through some key moments of the past decade as he’s been asked by Nigel Peaple to make sense of the current political situation, noting when you play fast and loose with economic frameworks you get a catastrophe that is politically driven by economic fear and worry.

He touches on politics from across the pond, and concludes that once in a lifetime events are very difficult to manage as you need to be ‘for’ things rather than ‘against’. Despite the previous successes of highly charismatic political people, populism has been moved aside and what we have seen now is a move to less charismatic, but certainly more stable personalities.

Now we’re on to the question that he’s been asked to answer: what would a change of government mean? His answer covers some key areas:

-

Reducing national debt — will be a number one priority for the next government

-

Europe — neither party will want to destabilise the current landscape and he thinks either party will be timid in its approach to Europe, but both will want to rebuild relationships.

-

Not raising taxes — no one will want to put more pressure on working people

-

Spending — there will inevitably be a fair amount of grappling with the pressure to spend more on public services

-

Growth — a sustainable plan for growth will need to be developed

-

Industrial policy — how to manage opportunities and risks whilst challenging investors to find the UK attractive

And that’s Ed. It was a shame there wasn’t more time for questions, especially given the number of hands that went up from the audience.

1.30pm

Last session before lunch, and now we’re looking at CDC. In the chair is the PLSA’s Rauri Grant. And he is joined by Jim Doran from Mercer, Simon Eagle of WTW and Phoenix Group’s Claire Altman.

Jim starts off by looking at whole of life CDC and discusses Mercer’s recent engagement and discussion with employers. He notes the ‘latent’ interest from some employers, especially larger ones. Some employers are attracted due to greater upside potential and downside protection, pooling of risk, and greater certainty. But there are concerns: member outcomes vs expectations, regulatory risk (especially acute as employers have been burnt by DB), cross subsidies, and complexity.

Simon responds by going through CDC at retirement only. Once a sceptic, Simon thinks whole of life CDC will be a niche offering, but sees greater potential in the ‘at retirement’ space. Sharing some results from a recent WTW polling of members and employers Simon notes how the results justify CDC decumulation only: 57% of employees want an income for life, but only 10% of DC members buy an annuity. 93% of employers think at retirement only CDC will be of interest to DC retirees. Simon concludes CDC needs work on the details but with robust mechanisms to determine benefits, strong governance, and excellent communication CDC decumulation is very attractive

Claire follows she highlights the need for scale, and is attracted to the role CDC can play in helping people at retirement. Claire asks whether there is a need for some form of compulsion to deliver CDC and, importantly, maintain scale. She also talks about managing member expectations and the importance of having well-trained call centre staff to help guide members.

Claire stresses the need for other options to be made available to members to ensure they are getting good outcomes, without the need for the sponsor to indemnify the risk. Speaking of risk, Claire also questions whether employers will voluntarily choose CDC unless there is some form of safe harbour and certainty that they won’t be on the hook.

Final thoughts conclude that the industry is grappling with multiple agenda items, and to get more movement on CDC we need to answer and address some key challenges. One of those being is inertia the right answer for decumulation, it’s clearly worked in accumulation.

12.34pm

We’re back after coffee and next up is a session on private credit and the green transformation of real estate, chaired by former Pensions Expert editor, now senior policy advisor at PLSA, Maria Espadinha. Maria is joined by Douglas Clark of Brightwell and Claus Skrumsager from Morgan Stanley Investment Management.

Claus takes us through the current environment of European real estate credit which is 80-90% owned by banks, but notes this is changing. It’s attractive in the current macro-economic environment as it mitigates interest rate and inflation risk.

Douglas tells us how Brightwell and BTPS have been investing in this asset class for over a decade, explaining why real estate debt can be attractive to pension funds. Douglas noted that it provides diversification, good returns and steady cash flows, with some very positive ESG credentials. But there’s also a couple of issues — it’s a relatively new asset class, with specialist providers so there can be higher fees, and there’s less data than other asset classes.

Claus focussed on the brown to green transition in the real estate market — 80% of existing European buildings will still be there in 2050, but much needs to be done to create energy efficiencies as 75% of them are energy inefficient. That transition needs an investment of €275bn annually!

11.00am

Firstly we hear the ‘what’ of pension funds acting for the public good. Adam tells us that there are three main priorities that pension funds have: pay the pensions of their members, grow the fund and make positive impacts. Luba says it has become clear that we cannot properly solve the problem of E without getting to grips with the S and G.

But ESG is so broad that areas to be thought about are almost too diverse, is that now a distraction for schemes who are swamped with reporting requirements?

We now move on to the ‘how’. Looking at assets holistically is the key to make sure they are acting for public good, the example given by Luba is airports, which IFM owns a number of. But looking beyond the investment to the holistic impact is something that they are looking at even partnering with airlines to develop sustainable fuel.

We’re now talking about scale and funding the transition by investing in emerging markets to support climate change objectives.

The panel is made up of open schemes, but what about closed schemes that are well on the way to their endgame? Are they thinking about the same private market investment options? Now we’re tackling some of the barriers schemes that stop schemes investing in private markets…size is the key. Both in terms of assets and time. The LGPS answer to this is pooling, but it’s noted that doesn’t happen in DB and DC – should it?

There’s a great discussion around the benefits of responsible investing, green investing, sustainability, ESG – no one is really sure how this should be referred to. When we open to the floor it’s more of the ‘when’ that is talked about. Should we just crack on? Yes. Of course we should. If only it was that simple…

10.00am

Good morning and welcome to day 3 of the PLSA’s investment conference. We’ll be continuing to give you snippets from the conference sessions throughout the day so stay tuned for the latest views and news. First up we’re talking about investing for the public good in the main auditorium.

The session is chaired by PLSA Policy Board chair, John Chilman, and on the panel is Gillian de Candole from Lothian Pension Fund, Adam Matthews from the Church of England, Luba Nikulina of IFM Investors and USS’s Innes Mckeand.

Day 2: Wednesday 7 June

5.25pm

And that’s it for the end of day 2 of PLSA Investment Conference 2023. A day that started with a peaceful protest was full of interesting insight and discussion. We hope we’ve given you a flavour of some of the topics that have been discussed. We’ll be back tomorrow bright-eyed and bushy-tailed for day 3.

5.20pm

Final session of the second day — what the asset managers say. We have a panel chaired by John Chilman with Iain Stealy from J P Morgan, Gavin Lewis of BlackRock and LGIM’s Sonja Laud.

Gavin opens the discussion, setting the scene on the key themes… consolidation across the board - DC, DB and LGPS, regulatory burdens and the role pension scheme assets can play in the wider economy.

Sonja says change is the only constant — regulatory change, geopolitical change. The shift in funding positions has left a number of schemes with the wrong asset allocation to support buy-out. ESG and pension scheme adoption of these principles can have a real impact on real world outcomes.

Iain is a specialist in international fixed income, for a long time his life wasn’t so stressful! Last year saw elements of his assets making double digit losses. We’ve seen right way correlation and wrong way correlation…bonds as a diversifier still work and they behaved exactly as they were supposed to. Iain is excited about the future, because history tells us when you get to the end of an economic cycle bonds perform best.

How do schemes get to their endgame? Iain notes the slow and steady nature of bonds, and also says liquidity is essential to get to buyout. Gavin thinks that many schemes’ positions have changed (and faster than they could’ve ever thought), but portfolio construction is still unique to each scheme. Sonja agrees and says only proper collaboration between the scheme, insurer and adviser will get the right result.

John directs the conversation to ESG, saying schemes do G well, the focus has moved to E… but what about the S and more of the E?

The panel discusses how to quantify the risk and opportunities. For the E this is a lot more advanced, but it’s still not perfect. Now the debate is about disinvestment and the exclusion of some asset classes, but that really does not facilitate the transition to a carbon neutral economy. Gavin talks about the S — saying there’s no real definition of what the S is, which makes measuring very difficult.

Final words from Gavin, powerful stuff: inequality gets in the way in the ability to manage the climate transition.

And with those words, we’ll close the blog for today.

16.10pm

What’s on the mind of Trustees? That’s what we’re talking about in this session with Anil Shenoy of Janus Henderson, Stuart Breyer from Mallow Street, Michael Chatterton from Tate & Lyle and Tegs Harding from Diageo — chaired by Nicky Day.

We open by looking at the top challenges trustees face - from a recent Mallow Street survey. 82% of respondents cited the increase in regulatory complexity as their number one priority.

The survey found the most material risk to pensions was underperformance of investments. There’s also a discussion around covenant — where weaker sponsors have an increased focus. The panel found it surprising that only 6% of respondents to the survey thought cashflow matching risk was most likely to impact their ability to pay pensions.

The panel quickly moved onto ESG, with discussion highlighting some of the main challenges as:

-

Added operational costs

-

Insufficient reporting from investee companies

-

Missing metrics

-

Lack of standardisation

-

Managers overstate ESG credentials

What else asks the chair? Separating the S from the E and G is where the focus of the conversation lands.

TCFD reporting gets mentioned, particularly who these reports are aimed at? The panel unanimously agreed that no member would read or understand that level of current TCFD reporting.

We’re now talking about ESG in DC, and the chair brings the focus to member engagement. She says she has a car, she has no idea how it works, but she doesn’t need to. So her challenge is why do the pensions industry spend so much time and effort in trying to make people understand the complexities of pensions.

Going wider, the whole panel agree on some key hot themes

-

Dashboards alone won’t solve understanding

-

Defaults need to be clearly explained

-

Pot follows member might work

-

Contributions need to increase

-

The auto enrolment starting age needs to be lower

-

Barriers need to be removed that are stopping people from saving

15.35pm

We’re back, after a longer than expected lunch, in the DC stream to talk about modern investment design for decumulation.

The PLSA’s Alyshia Harrington Clark is in the chair, with Julian Barker from DWP, Cardano’s Stefan Lundbergh. L&G’s Jestral Mistry, and Lee Hollingworth from Franklin Templeton.

Julian leads the DWP’s policy work on decumulation and CDC. Certainly a hot topic. The response to the decumulation call for evidence will be published in the summer. DWP is considering putting a duty on trustees to take into account the needs of members at the point of decumulation. This won’t be prescriptive, but there will be an expectation that members have an expected option. This won’t be a ‘default’, as choice is important, but DWP wants an expectation to be created for members. Julian finished by saying that the minister is really interested in managing risk and volatility during the ‘at retirement’ phase, and is keen that, “in time”, a CDC product will be available to all members.

In response, Lee noted that solving the decumulation problem is very personal to the member. There is a need to segment the population — people are going to need to make their money last as long as possible, but most won’t be in the position not to draw on capital. Lee argues that some form of default pathway dependent on pot size and depending on other characteristics might be a way forward.

Jestral stresses the need to think about the end outcome for members. The biggest challenge is understanding what members need, but this will change over time. The investment problem was easier to solve in a world where members were targeting an annuity. There is a mismatch between when people actually take their money and when they plan to. This uncertainty makes things difficult from an investment perspective. Jestral also floats the idea of whether a default approach should be considered.

Stefan notes that a lot of investment thinking is based on defined benefit rather than defined contribution. He highlights the disparity in contributions between DB and DC schemes and the consequences of that for the viability of securing a long term income. Stefan highlights that policymakers are fixated on a fixed retirement date and questions whether aggressive derisking leads to optimal outcomes. He argues that we need to leave the “old thinking behind”, and queries whether politicians are trying to solve yesterday’s problems.

A good discussion ensues on the panel on Collective Defined Contribution and its potential to be part of the at retirement solution. Stefan coins the phrase “Complicated DC” — we wonder if that will stick?

Time for coffee!

12.50pm

Net Zero meets reality with James Walsh, (Chair), Andrew Parry (J O Hambro Capital Management), Will Martindale (Cardano), Giulia Chierchia (BP)

We kick off this net zero meets reality session by acknowledging that passions about climate change are growing, the science is becoming more robust, and more voices are talking about it — a perfect example being the protest that welcomed delegates this morning.

This is a complex topic that is multi-dimensional, presenting challenges and risks along with opportunities to fund the transition. A key point highlighted is how policy is the catalyst that will tilt the flow of capital to fund the transition.

The panel discuss that, to achieve net zero, it’s the highest emitting industries that need to make the biggest changes. And that requires better energy networks to support the work of the high growth companies, like Microsoft.

Andrew talks about energy networks and says that 55% of world renewables will be coming from China in 2024. This means that the transition becomes a geopolitical competitive market — a great opportunity for investors.

A quick audience poll reveals 87% of the audience say their scheme is currently invested in oil and gas.

Giulia explains that the Ukraine war triggered an energy crisis that we can’t ignore, but, like it or not, we can’t unplug fossil fuels from our existing energy network. We need to invest in both to maintain economic output and growth. To keep pace with energy needs, she highlights that £400-450bn of investment is needed in oil and gas on an annual basis (assuming a net zero trajectory). But if we’re not on a net zero trajectory, that needs to go to £700bn investment per year). Strikingly, Giulia notes that we also need £4trn invested into renewable energy — every year — to meet climate goals while maintaining energy outputs.

Giulia says that there are currently 12 million EVs globally today. However, this needs to increase to 2 billion to meet the net zero goal — demonstrating the opportunities for investment in the transition.

There’s a cheeky comment asking if BP will rebrand to British Energy!

Another ask the audience - does your scheme instruct fund managers to vote on climate-related resolutions - 55% say yes, 32% don’t know.

Will from Cardano takes a look at the practical steps schemes can take to move to net zero:

-

Think about decarbonisation framework

-

Think about the different investment options available

-

Think about a stewardship policy

-

Think about communicating to members your plan for decarbonisation

-

Think about your power of influence

Will says in an ideal world we’d regulate corporates, asset managers and then pension schemes to report on net zero. In the UK we’ve done this back to front.

12.26pm

Accessing private markets in DC

So what did our panellists have to say about the opportunities, and barriers, for schemes investing in private markets?

Anne Lester from Partners Group stresses that there is a natural cap on allocation to certain asset classes within an overall multi asset portfolio. Anne also talks about the importance of scale with examples from the Australian Supers. She notes that private markets are a terrific place to explore ESG — by definition schemes can be far choosier about where they can invest their money in line with their beliefs. And there is the potential for impact investment, eg solar, wind etc.

J P Morgan’s Renne Poisson adds that investment in private markets allows access to non-correlated returns and access to the liquidity premium. They are also more in line with the modern economy where companies are staying private for longer — so if schemes don’t consider private markets then they are narrowing the opportunity set for investments. Renne also makes the point that private markets are expensive, and the use of performance fees, if structured in the right way, can create an alignment of interest.

Joshun Sandhu from Mobius gives the platform perspective and how best to manage illiquids in DC. Mobius’ experience from DB has informed thinking for DC, and it’s been a journey starting with more liquid assets and moving to less liquid assets. Joshun notes that the LTAF structure takes away some of the regulatory barriers from investing in illiquids, particularly around permitted links, but operational challenges still remain. The approach being adopted to ensure liquidity is to blend the LTAF alongside more liquid assets.

LCP’s Stephen Budge starts from the member perspective and delivering better outcomes. Stephen asks the key question is how can schemes maximise opportunities for members. He notes that if schemes aren’t accessing private markets then they are potentially missing an opportunity. Stephen comments on the Government’s push to get schemes to invest in UK growth assets and believes that work so far has increased understanding of the issues and is helping to remove barriers to investing in this asset class. He also notes the need to ensure fair valuation of assets, particularly given the need for daily trading in the DC environment.

11.47am

We’re back and refreshed after the latest coffee break and we’ll be covering two sessions in the live blog…. multitasking!!

So stay tuned for some chat about private markets in DC and net zero meeting reality.

10:45am

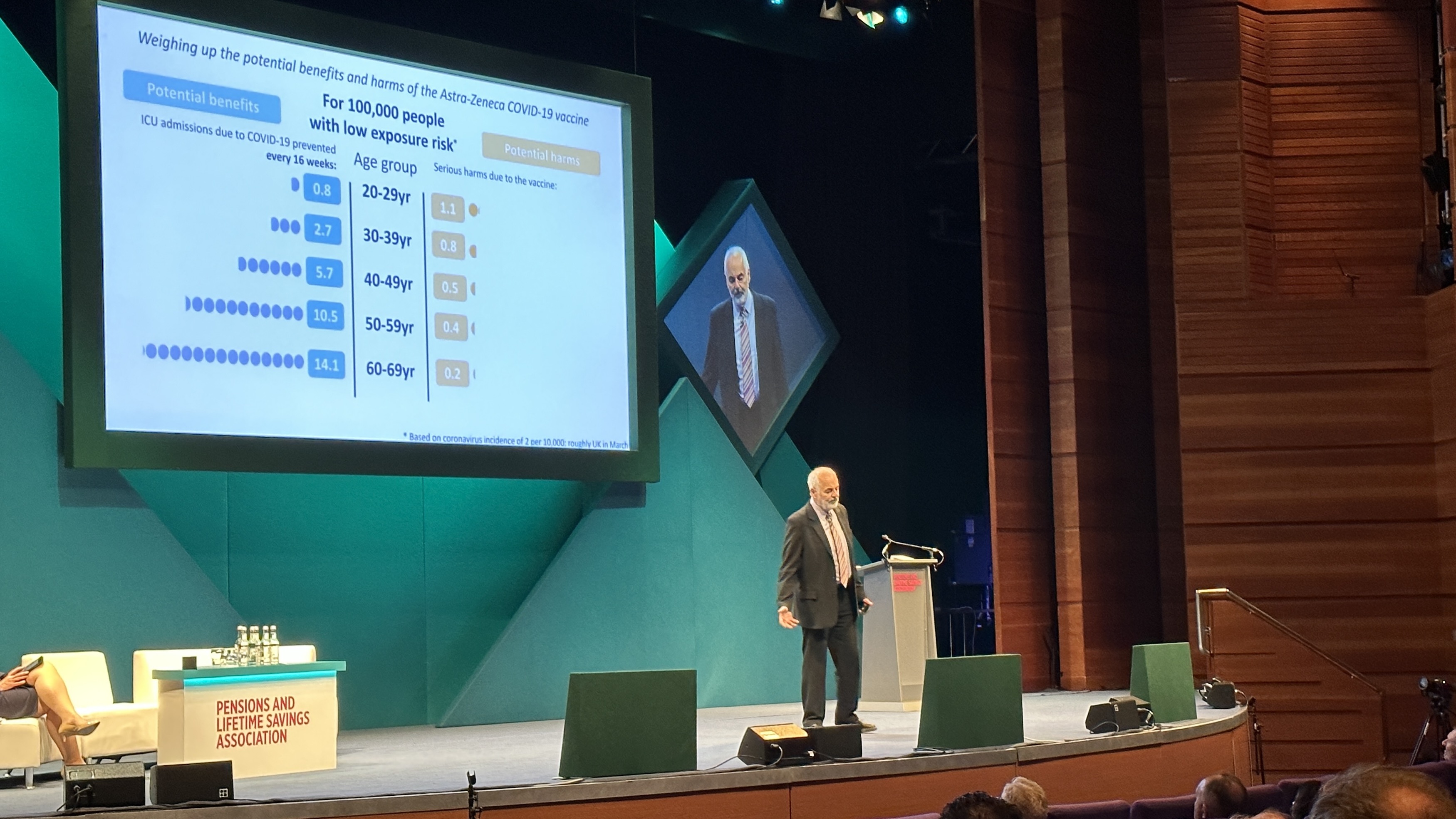

Should we trust claims about risk?

Annnnnd we’re back. The first session in the auditorium kicks off with a lively presentation by David Spiegelhalter, a statistician.

He flies through example after example of what he calls ‘number theatre’ where real research reports are spun… making them more attractive to read, but changing the real findings.

The talk culminates by honing in on delivering trustworthy communications, saying that organisations should not be asking how to increase trust, but how they can deliver communications that demonstrate trustworthiness.

He outlines five rules to evidence communications:

-

Inform, not persuade

-

Balance, but not false balance

-

Disclose uncertainties

-

State evidence quality

-

Pre-bunk misinformation

09:00

The conference doors are open — on the walk in we hear a chorus of “fossil fuels must go go go”.

The polite protest is a group of environmental activists calling for the end of investment in fossil fuels. No angst, just a clear and simple message…

Day 1: Tuesday 6 June

6.25pm

That’s a wrap for today and the end of the formal proceedings. Next up are the conference drinks…and your Pensions Expert team will be making the most of these.

Until tomorrow!

6.20pm

Hopefully you’ve stayed with us for the final session of the day — changing expectations for LDI.

Our panel certainly had a range of experiences and plenty to learn from the scale of the challenges faced by trustees in autumn 2022.

The causes of the LDI crisis have been well documented and the panel noted that it wasn’t the rise in yields that was a problem it was the speed — and the need for decisions on asset allocation to be made at an unprecedented speed. It was noted that in some cases trustees didn’t have sight of everything and decisions may have been made and then the trustee was blindsided.

The panel thought that those two weeks in autumn 2022 highlighted various weaknesses and issues within scheme governance and the ability to react at speed.

So, with the benefit of hindsight what does the industry need to look at:

-

Improved modelling

-

Improved risk management

-

Operational efficiency

-

Broadening of LDI investments

-

Strengthening governance, communication and decision-making process

Overall, managing investment and non-investment risk is key. Discussions should be actively taking place now and plans being put in place to deal with the next crisis.

17.35

Back from coffee (or gin for some) we now hear from the CIOs of some of the largest pension schemes in the UK in the new paradigms for a new investment climate plenary.

There’s a lot keeping them awake at night, with CIOs of DB, DC and LGPS schemes all grappling with different scenarios, but all dealing with the fallout from last year’s gilts crisis and the current macroeconomic and geopolitical uncertainty.

The panel picked up on Danny Blanchflower’s pre-coffee session, with comments made around the fact that the UK is a large open economy so it’s not immune from global shocks, and that the degree of relative instability in policy making requires a risk premium.

The panel also noted that when the current wave of inflation moves through the index we need to be aware of what economic regime we are moving into — low inflation and low rates or higher and more volatile inflation. This will be key to building an investment portfolio.

In terms of key challenges, there’s far too many to cover in this live blog, but here’s a taster of the whirlwind tour from this panel:

-

Nest’s net performance goal is CPI +3% after all charges. This is ok when inflation is low single digits, but at current rates it is a lot more challenging.

-

Any form of investment mandation is a worry — need to let markets play out and not be biased for or against the UK.

-

Does more domestic investment make sense? There are more key influences in play now. Domestic investment less exposure to geopolitical risk?

-

When a scheme is in surplus… is it all plain sailing? No. Evaluation of the strategy to keep the surplus and avoid dropping back into deficit. A surplus needs to be thought about in layers or buffers, using risk return trade offs.

-

Schemes need to look bigger than just the equity part of the investment stack. Investors are really uncomfortable with uncertainty — forecasting is a key part of being able to commit capital, so when the government introduces sudden windfall taxes it’s really unhelpful.

-

Any long term UK investment vehicle should be as attractive to overseas investors. The returns must stack up.

Also, the NEST representative gave a hint of what may be to come later in the year with the DWP’s expected policy paper on decumulation, noting that “How to get the best income in retirement for people is on the agenda for this year.”

3.47pm

And now we break for a much needed coffee, although after Danny’s talk some in the audience might need something a little stronger. We’ll be back a bit later, so stay tuned!

3.35pm

Now a change of tack, with Professor Danny Blanchflower talking economics — a talk about history, where we are now, and where we’ve been.

Danny is his usual controversial self and is brave enough to mention the ‘B’ word (Brexit for the avoidance of any doubt) in relation to the UK’s economic and inflationary performance vis a vis other countries.

In summary, Danny questions the Bank and its forecast based on interest rate expectations: “they’ll kill off inflation, they’ll kill the economy off, they’ll kill off growth, and there’s a not insignificant probability of deflation”.

3.05pm

Reaction already coming in to the city minister’s speech. Phil Brown, director of policy at People’s Pension, and one of the esteemed panelists mentioned below has commented:

“Any initiative to encourage pension funds to invest in UK infrastructure and business must be done with the savers’ best interests in mind.

“To achieve this, we think that either an Australian-style fund and member favoured asset manager or a pooled asset vehicle are approaches that should be explored. However, there is also a need to focus on the size of asset funds in the market being of the necessary scale. One way of doing this could be further consolidation of the Defined Contribution market, although this is not the only option.”

No doubt this will be a debate that will rumble on and on through the conference.

3.00pm

An esteemed PLSA panel debate the minister’s words.

Four words best sum up the panel debating the issues picked up by the minister’s speech: consolidation, consolidation, consolidation and scale.

The whole panel agree that mandation is not going to drive the right behaviours or outcomes. The fiduciary is the bedrock to our pensions system.

PLSA policy board chair, John Chilman, says he “completely supports mandation”…. But, and it is a big but… “only if the government underwrites it”!

Comment from the floor — the ‘n’ word hasn’t been mentioned…are we not talking about nationalisation of our pensions system? Also from the floor, is the government the natural consolidator for DB schemes?

2.25pm

Next up is a view from government, with Andrew Griffith MP, economic secretary to the Treasury and city minister, delivering a pre-recorded speech.

Andrew’s been an MP since 2019 and has been in post for 6 months — with a broad remit — Financial Services Regulation and Pensions Tax.

His short speech congratulates the PLSA for marking their centenary, helping people achieve a better retirement income for 100 years.

In brief, Griffith said:

-

The government’s focus is more on performance and less on cost.

-

He believes in savers and saving as a principle. The government wants to reward risk-takers and savers, as shown by abolition of the LTA.

-

He believes it’s in savers’ interests to investigate the opportunity of illiquid assets.

-

The government is not only looking at building scale for private sector DC and DB schemes, but is also looking at the LGPS.

-

The philosophy of government is to make the UK attractive and make investing in UK growth attractive and appropriate for UK pension funds.

2.15pm

PLSA chair, Emma Douglas, sets the scene for this year’s investment conference. She thanks attendees for showing commitment to the PLSA, the important work that the industry does together, and the dedication to helping everyone achieve a better income in retirement.

Douglas takes a quick canter through the issues that the PLSA has been involved in from pensions dashboards to ESG to the DB funding code to CDC and much more.

Douglas highlights the current live debate around pension fund investment — a debate that is focussed around the possible mandation of pension fund investment in the growth of the UK economy.

PLSA policy board chair, John Chilman, has been involved in roundtables with the Chancellor and Douglas stressed that the PLSA supports investing in UK growth, but where the aim is to achieve the best outcomes for savers.

The PLSA has identified a number of ways that the government can take action to encourage more investment in the UK by doing more to increase the right kind of investment opportunities by, for example, changing the regulatory and fiscal regimes.

2pm

Waiting in anticipation for PLSA Chair, Emma Douglas to kick off PLSA IC2023.

1.00pm

We’ve arrived in Edinburgh at the EICC. Delegates are starting to pour in ready for the conference to start in earnest at 1.00pm, with, well, lunch!

Stay tuned as we bring you the latest news and views from PLSA IC 2023.