Johnson Matthey Pension Scheme has reduced its deficit by around £145m after taking a raft of measures to address its funding shortfall, including the creation of an asset-backed contribution vehicle comprised of third-party bonds.

Low gilt yields and the resulting higher pension deficits have forced novel approaches to funding across several schemes, such as the use of asset-backed contributions. Earlier this year, retailer Morrisons placed £150m of property assets in a special purpose vehicle to secure its scheme.

SPVs are a legal entity into which employers can place a range of assets to bolster a pension fund. These are often in the form of property or company brands, but schemes are exploring other asset types with a low correlation to their sponsor’s covenant.

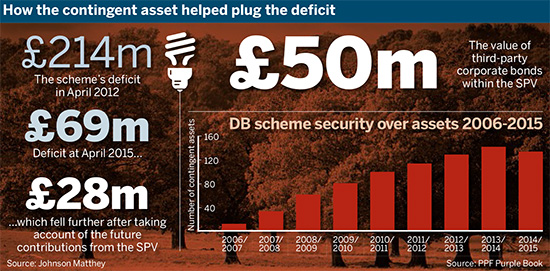

Johnson Matthey, a sustainable technology and chemicals company, had a scheme deficit of £69m at April 1 2015, down from £214m on the same date in 2012, according to its most recent results.

However, the deficit fell further to £28m “after taking account of the future additional deficit funding contributions from the special purpose vehicle set up in January 2013”.

Diversified assets

Johnson Matthey’s SPV was set up with £50m of third-party corporate bonds, from which the annual income will be paid to the scheme while it is in deficit. This is in addition to the £23.1m annual employer contribution that will be paid until 2020.

Other derisking moves by Johnson Matthey

Johnson Matthey closed its career average defined benefit scheme to new entrants in October 2012 in favour of a new contributory cash balance DB scheme, and increased employee contributions for those who were still accruing benefits.

In 2013/14, the scheme introduced a hedging programme to reduce its exposure to interest rates and inflation.

Hugh Nolan, chief actuary at consultancy JLT Employee Benefits, said it was unusual for a scheme to invest third-party bonds in an SPV, as typically they use assets they already own, such as real assets or branding.

He said: “I’ve not come across that myself yet… it’s not money that’s swallowed up if the scheme does well. It might just be an effective way of doing an escrow approach.”

Vicky Carr, partner at law firm Sackers, said that in the case of SPVs, while “the trustees take an investment and that partnership interest has value”, therefore increasing the assets of the scheme on the balance sheet, it can still be in some ways reliant on the employer.

For example, the Pensions Regulator’s guidance on asset-backed contributions warns schemes “may not be entitled” to access the assets in the partnership “and may have to rely on another party – for example, the general partner [of the SPV] – to enforce the obligations”.

But Jonathon Land, partner at consultancy PwC, said schemes setting up SPVs should be conscious of the assets being used as some are more beneficial than others.

“The diversity of the things that are going into SPVs are changing all the time,” he said. “The more you can differentiate the asset that’s in it from your employer covenant the better.”

He added that assets like property could be desirable for an SPV because they are not linked to a business’s strength.