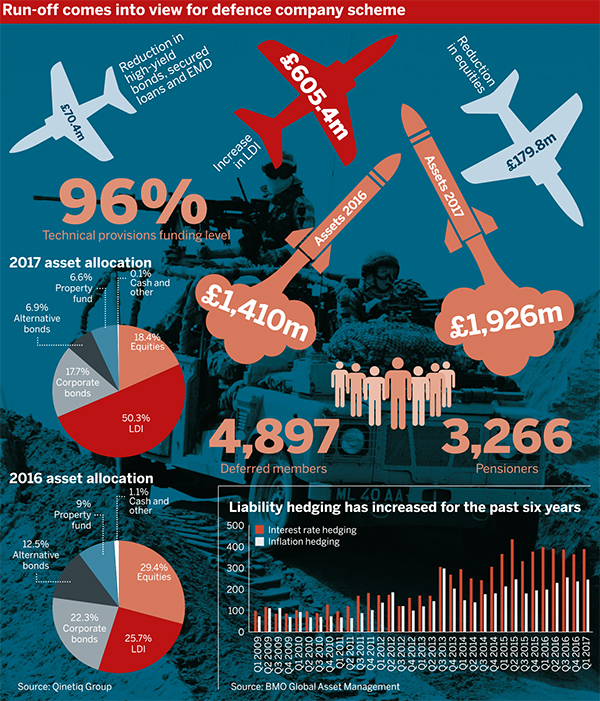

The Qinetiq Pension Scheme has seen a £605m boost to its liability-driven investments and has begun discussions over its long-term future as it nears full funding.

As schemes mature and look to safeguard funding levels, many continue to move to LDI solutions. An update by BMO Global Asset Management found that in the first quarter of this year, total interest rate hedging was up 7 per cent compared with the last three months of 2016, and inflation hedging was up 4 per cent, mostly because of pension funds using LDI.

That’s the biggest driver that we see of overall funding position, whether or not the scheme has embraced LDI early

Barry Jones, KPMG

The £1.9bn Qinetiq scheme’s LDI portfolio – consisting of hedging instruments, synthetic equities and liquidity – rose by £605.4m over the year to March.

Most of this steep increase was down to valuation gains, but the fund also pulled £179.8m out of equities and £70.4m out of high yield bonds, secured loans and emerging market debt.

Group pension and benefits manager Andrew Gibson said the scheme’s triggers mean the LDI portion gets a boost whenever the funding level is up a further 2 per cent. On a technical provisions basis, the scheme is now 96 per cent funded and has tipped into surplus on an accounting basis.

The derisking happens automatically. Gibson said a risk analysis tool the scheme has had for about a year tracks the funding level and sends an automated message to LDI manager Insight Investment.

“Once that’s hit, messages go round, there’s a check that Insight do, and if it passes that we derisk,” Gibson explained.

Run-off comes into view

As the scheme nears full funding, the end game is coming into focus.

“We’re just thinking now, okay, what’s happening over the next 20-30 years with the run-off, and yes, buy-in, buyout is an ultimate goal,” said Gibson.

However, “I’m not sure we’re close to that yet… we’ve still got a fair bit of work to do. We’ve done a lot of work with our administrator in tidying up the pensioner data, making sure we’ve got all the spouses’ and other information that insurers would want to see”.

Other factors are also at play when determining whether buy-ins or buyouts are attractive.

David Felder, director at Law Debenture Pension Trustees, said: “The first thing to look at is the split between deferred members and pensioners. Buyouts become viable when members are pensioners, and buy-ins become viable for the pensioner population before that.”

The scheme, which closed to accrual in 2013, has a split of roughly 60 per cent deferreds to 40 per cent pensioners.

In terms of LDI triggers, Felder advised to use a time-based mechanism: “You say that over a two-year period, we intend to increase our hedge ratio to whatever the target is... and should yields increase faster than expected we might accelerate our programme and conversely, if interest rates fall away... we’ll actually slow down a bit.”

LDI crucial for funding level

Qinetiq’s funding level was likely helped by a switch to the consumer price index for increases to accrued pensions, confirmed by the Court of Appeal last year after the High Court had approved it in 2012.

Barry Jones, senior manager at consultancy KPMG, said a switch to CPI from retail price index can lift a scheme’s funding level by up to 5 per cent.

John Lewis Partnership protects future with LDI

The John Lewis Partnership Trust has introduced a liability hedging programme increasing its hedge ratio to 60 per cent, in a move experts said would protect significant recent contributions.

The John Lewis Partnership Trust has introduced a liability hedging programme increasing its hedge ratio to 60 per cent, in a move experts said would protect significant recent contributions.

However, the single biggest determinant for how well a scheme is funded is how early LDI was taken on board, he added. “Broadly speaking, that’s the biggest driver that we see of overall funding position, [it] is whether or not the scheme has embraced LDI early,” said Jones.

Schemes continue to shift assets towards LDI. KPMG’s latest survey found “relentless growth” in the sector, said Jones.

Maggie Stoker, client director at professional trustee company Capital Cranfield, said LDI can be useful for schemes that want to cap their deficits, but cautioned that liquidity needs to be managed carefully.

“My issue sometimes with LDI is, it’s great for keeping the finance director happy because they’ve got a degree of certainty… but the other side of the coin that one needs to consider is cash flow generation,” she said. “LDI doesn’t necessarily guarantee having the cash to pay [a pension]”.