The trustee board of Lafarge’s UK pension fund has begun discussions with its sponsor to ensure members would be protected under its proposed $40bn (£23.8bn) merger with Holcim to form a global cement maker giant.

The recovering global economy has seen renewed merger and acquisition activity in the building and pharmaceutical sectors, and employer covenant experts have urged schemes to keep their sponsor close to avoid the security of their benefits being threatened.

"Your trustee board has initiated discussions with Lafarge to ensure that the security of members' benefits will not be adversely affected by the proposed merger," the scheme told its members through a message on its website. The scheme promised to update members in due course on further developments.

A spokesperson for the parent company said it was "way too early" to comment on the impact the merger could have on the Paris-based multinational's UK pension fund.

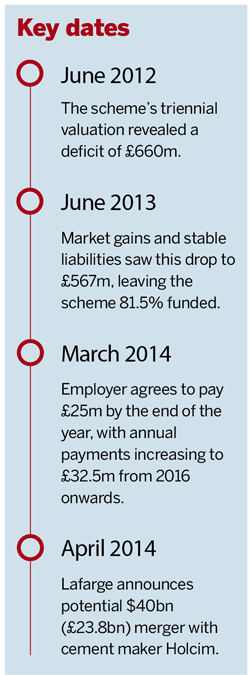

The merger proposal was announced only weeks after the scheme secured a funding deal with its sponsor to more than double its employer contributions, as part of a beefed-up recovery plan to achieve annual payments reaching £32.5m from 2016 onwards. This will be well above the £12m contributed between 2010 and 2012.

Defending scheme benefits

The Pensions Regulator requires trustees to identify whether any proposed corporate deal could represent a type-A event, which means it is "materially detrimental" to the scheme's ability to meet its liabilities.

This could be the case if the deal involves the taking on of debt that pushes the scheme down in the creditor priority list.

Aidan O'Mahony, a partner in the covenant assessment team at consultancy Aon Hewitt, said pension fund trustees of a UK pension fund sponsored by a global parent caught up in M&A activity needed to "rattle the cages" to make themselves heard.

"It is really just to get a foot in the door and register their interest," he said. "The first thing the trustees can do is flag their interest to management and get it on record that they are a creditor."

Often schemes and employers will look to find a 'sweetheart deal' to avoid the regulator stepping in, with trustees requesting a shopping list of assets or guarantees to improve the covenant strength. "Number one [on the list] is cash now, number two is cash tomorrow," said O'Mahony.

Simon Kew, director of pensions at specialist covenant assessors Jackal Advisory, agreed it was crucially important for trustees to have laid the groundwork before any merger or takeover activity is announced.

He said: "The best thing they can do is have a good relationship and a good dialogue with the employer and look at protecting members benefits on a 'what if' basis beforehand."

Kew warned that while a scheme could benefit from an incoming company that is looking to buy the scheme off the balance sheet, such intentions may not last. "Just because the incoming company is playing ball now it does not necessarily mean they are going to be playing ball in future," he said.

Richard Farr, partner and leader of the pension business advisory team at consultancy BDO, said schemes needed to consider three things: their current covenant position, whether the prospects of their sponsor has changed, and what powers they have as trustees.

He added: "You obviously ask for mitigation, you ask for compensation – you may get more than you need."

One power that the scheme has is to reflect a weaker covenant by derisking the scheme's investment strategy, resulting in lower investment assumptions and a greater deficit burden.

"Clearly you won't change your investments immediately when the deal happens but you can assume you will. It is a chess game."