Consultancy KPMG is looking to group small schemes together before bringing them to the bulk insurance market, allowing them to better access the buy-in and buyout markets, but rivals have said governance could prove a challenge.

The bulk annuity market has been growing, with nine insurers announcing deals in 2015, up from seven in 2014, and speculation that deal volumes could reach £20bn, from £11bn last year.

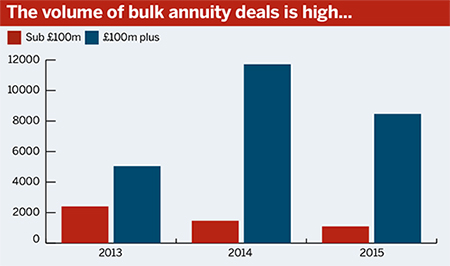

Although the volume of bulk annuity transactions has been growing, the number of transactions has been falling and falling

Tom Seecharan, KPMG

Tom Seecharan, director of pensions insurance at KPMG, said the consultancy is planning to carry out the first transaction in Q4 this year.

“The critical thing is having enough schemes together to get critical mass,” he said.

Criteria for grouping

The consultancy will look for schemes or sections of schemes smaller than £50m. It aims to complete transactions on between £50m and £150m of assets, including five to 10 schemes each time. Seecharan said the company is currently in talks with eight schemes.

He added there were 187 sub-£100m transactions in 2013, accounting for 30 per cent of total market volume. However, there were fewer than 90 up until the end of Q3 2015 and they accounted for just 10 per cent of market volume in 2014 and 2015.

![]()

“Although the volume of bulk annuity transactions has been growing, the number of transactions has been falling and falling,” Seecharan said.

Alignment challenge

Jerome Melcer, director at PwC, said that while it is not uncommon for a sponsor with multiple schemes to complete a transaction, he is not aware of any such transactions for groups of schemes that do not share a sponsor.

“[The] challenge is one of governance. They’re talking about multiple trustee boards and multiple sponsors. [There is the danger of a] possible misalignment in terms of what they’re looking for in a deal.”

He added there were a number of factors that could scupper a deal, such as the timing of the transaction and which insurer was carrying it out.

“If you’re trying to strap schemes together, you’ve suddenly increased your [potential] failure rate. It only takes one scheme to say, ‘You know what, this isn’t right for us’.”

Melcer said there are ways to improve the experience of smaller schemes, but admitted size is a factor when determining the likelihood of making a deal.

“There’s a sweet spot. If the deal is too small you just won’t get the time. If it’s a big enough deal they might enter the process. If a deal is too big, you start shrinking interest because of the amount of capital that would need to be tied up.”

PwC uses scheme data on its Skyval platform to provide pricing models to insurers, with the aim of saving them time that would otherwise be used modelling the scheme liabilities to provide a price and would not necessarily guarantee any business for the insurer.

Chances of an individual transaction

Charlie Finch, partner at consultancy LCP, said small schemes can transact if they can convince insurers that it will be a swift and smooth process.

“Our view is, for smaller schemes the best way of making sure you get traction… is all about how you approach insurers, demonstrating you are likely to transact quickly, easily and efficiently,” he said.

He added LCP was not looking at aggregating schemes to bring to market as KPMG is, due to the difficulty in aligning all parties involved.

David Ellis, partner at consultancy Mercer, said not all insurers target the same size of schemes. “Some of the insurers coming to the market are particularly interested in small plans,” he said.

However, he added: “There is a problem getting multiple trustees to all do a deal at the same time.”