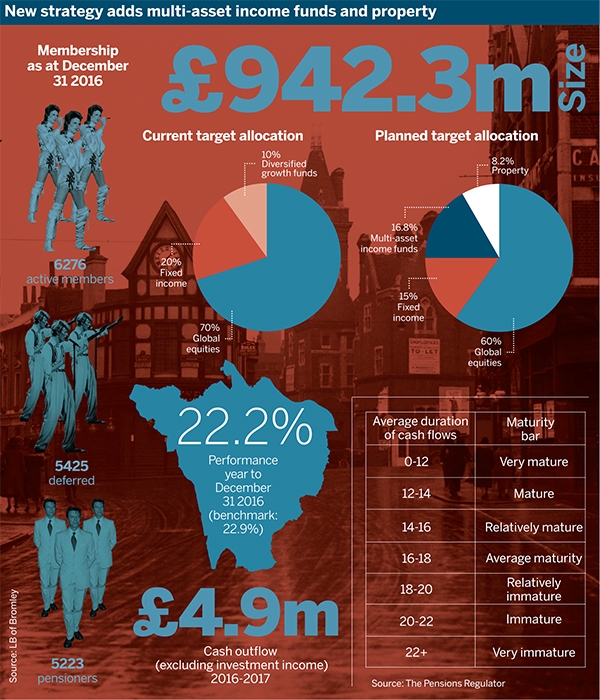

Faced with a projected cash outflow of nearly £5m in 2016-17, the London Borough of Bromley pension fund is trying to keep income up with a new investment strategy.

The Local Government Pension Scheme as a whole is thought to have tipped into cash flow negative territory if investment income is excluded, with London funds particularly affected. This is due to a larger number of pensioners and lower numbers of active members – partly because of austerity cuts.

That’s the whole point of having a funded scheme – you put the money aside now to pay for pensions later

Graeme Muir, Barnett Waddingham

While more schemes are expected to adjust their investment strategies to generate income, Bromley is an early mover.

Principal accountant James Mullender said the fund is seeing greater cash outflows than inflows when excluding investment income.

The £942m scheme has therefore agreed to swap a 10 per cent diversified growth fund allocation with around 16.8 per cent in multi-asset income funds.

It is also creating a circa 8.2 per cent UK property allocation, cutting equities to 60 per cent and fixed income to 15 per cent.

The fund’s advisers Allenbridge had originally proposed a much higher property target of 20 per cent, and only 5 per cent in multi-asset income funds, but the scheme preferred putting less weight on property due to its liquidity profile, said Mullender.

“When they’re both projecting similar rates of return… they’d rather go more liquid,” he said.

More schemes will follow

More pension funds will start to look for investment income now, said Graeme Muir, head of public sector at consultancy Barnett Waddingham.

He highlighted that some might say pension funds could simply take the investment income their current strategies generate. However, this might not always be possible in practice as not all investment funds have income units.

“With some of these arrangements it’s not quite so easy, [investors] might be almost locked into a unit where it automatically gets reinvested and there is no actual scope to get it in cash,” he explained.

Muir stressed that using up assets is a natural part of the lifecycle of a pension fund: “That’s the whole point of having a funded scheme – you put the money aside now to pay for pensions later."

He said as long as a fund is not losing too much total expected return, moving to a more income-based strategy should not create any issues.

Multi-asset income v DGFs

Danny Vassiliades, managing director at consultancy Punter Southall, agreed the question of how to take income will dominate over the coming decades.

“A clear disinvestment plan is needed” if schemes are to avoid being forced sellers, he said.

He explained that the underlying assets in multi-asset income funds tended to throw off more income per unit than those in DGFs.

Whereas DGFs are trying to give a smoother total return, the multi-asset income fund will be holding assets such as fixed income or property.

Stagecoach chair stresses need for accurate cash flow data

Accurate data on scheme balance sheets and a willingness to seek out information independently of consultants and advisers is crucial to managing a scheme facing changing cash flows, the chair of the Stagecoach Group Pension Scheme said.

Accurate data on scheme balance sheets and a willingness to seek out information independently of consultants and advisers is crucial to managing a scheme facing changing cash flows, the chair of the Stagecoach Group Pension Scheme said.

Vassiliades said a larger scheme could tolerate 15 per cent to 20 per cent of illiquid assets, but added that some caution is needed nonetheless.

“They have to be careful because with pension freedoms there’s a lot more transfer value traffic,” he warned.

No infrastructure target

Bromley has not included an infrastructure target in its new strategy, despite the government’s aim of getting LGPS funds to invest in this area.

Muir said that while pension funds would like to have infrastructure assets, they generally would not take on the risk of building infrastructure without a guarantee from the government.

“They will buy infrastructure once it’s built,” he said.

Vassiliades pointed out that infrastructure is illiquid, posing another long-term challenge for LGPS investment.

“Eventually, while there is scope for infrastructure investing, at some point the local authority and other funds might just turn around and say, ‘We can’t tie up the money in infrastructure’.”