BP Pension Scheme has formalised a derisking framework with its sponsor to dampen covenant, asset value and investment risks, delegates at the National Association of Pension Funds’ investment conference 2014 heard last week.

Sally Bridgeland, chief executive of BP Pension Trustees, said the scheme began looking at derisking in 2011 but is still on a path to find the right investments and capabilities to match future liabilities, which are expected to be more than £20bn.

BP's key risks

Covenant impairment

Asset value impairment

Investment income impairment

Implementation of investment strategy risk

Strategic, operational, controls and compliance risks

“We had 2008, when our asset values had gone down a lot, and we had 2010 when we had what can be described as a ‘covenant event’,” she said, adding that this revealed the high risks facing the scheme.

In 2010, the oil company had to deal with the fallout of an oil spill at its Deepwater Horizon rig in the Gulf of Mexico, which hit its share price.

Discussions with the sponsor focused on devising a plan that got the scheme to a “sensible place in a sensible timeframe”, where the risks faced, should the covenant, asset value and investment income become “impaired”, were better suited to the fund’s liabilities.

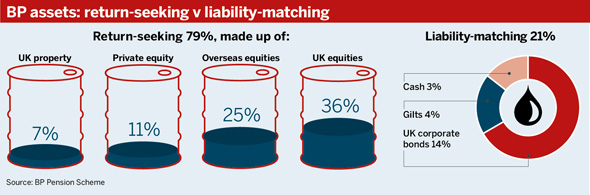

The scheme has 79 per cent of its portfolio in return-seeking assets, which means the probability of asset value risk is high, Bridgeland said.

She stressed the importance having a long-term legal agreement in place that sets out yearly contributions, how the deficit is calculated, and the assessment of the derisking path.

“The sponsor underpinning the investment risk was actually very important for us,” Bridgeland said.

The aim of the derisking plan is to mitigate the impact of becoming cash flow negative and hinges on three main points:

Aligned income – improved connection between investment income and members benefits.

Stronger balance sheet – reduced reliance on investment growth and the sponsor.

Refocused capabilities – ability to make investment decisions focused on progressively improving benefit security.

“We still have money coming in from the company and from investments. For the next 10 years at least we expect to be cash flow positive,” Bridgeland said. “So the impact of having not as high a balance sheet as we would like to have to run a lower-risk investment strategy is not as extreme as if we were cash flow negative.”

The scheme will ultimately move from growth-seeking assets to liability-matching assets.

For the next 10 years at least we expect to be cash flow positive

Growth versus matching assets

Bridgeland questioned whether the scheme could create an investment strategy where the growth assets could morph into liability-matching without having two separate buckets.

“[And] if necessary, creating the technology and systems that will help you see farmland, infrastructure and emerging market debt as similar kinds of investment – that have cash flows and different kinds of risks that you can put together in the right kind of product [to match liabilities],” she said.

Glyn Jones, chief investment officer at fiduciary manager P-Solve, told delegates derisking plans up to now have been applied in an overly prescriptive way.

"It needs to be more pragmatic and more flexible. It needs to have the ability to react to events," he said.

Jones suggested schemes identify where they are going and put in place a framework to get to that point – but warned not to derisk too quickly.

"One of the worries is that slowing down too soon could be fatal for pension schemes," he said.

Schemes should be clear about what risks they are trying to manage, and should consider what should happen if things are better or worse than expected.