Pension schemes compelled last year to derisk at historically low yields quadrupled the previous year’s gilt purchases, according to official data that have left investment experts surprised.

Low-yielding gilts have forced some schemes to seek alternative assets in order to hedge liabilities. Last week the Daily Mail and General Trust scheme said the price of index-linked gilts had forced it to look elsewhere to match liabilities.

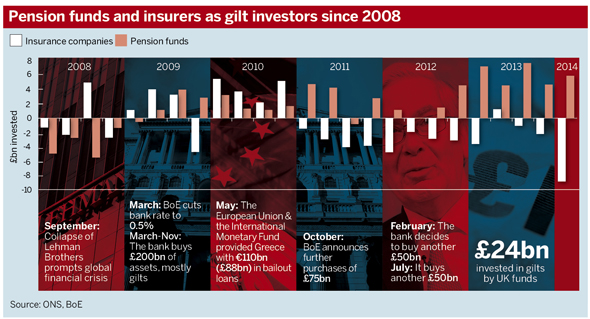

But data released on Thursday by the Office for National Statistics showed derisking continued apace last year despite value concerns.

The ONS’s estimated inflows for last year show schemes ploughed £24bn into both fixed rate and index-linked gilts. This is compared with investment of £7.2bn in 2012 and £11bn in 2011. This is in stark contrast with insurance companies, which have disinvested more than £30bn from the start of 2011 to the end of 2013.

The trend looked set to continue with schemes investing nearly £6bn into gilts in the first quarter of this year, while insurers sold off almost £9bn of the asset class.

Nicola Ralston, director at investment consultancy PiRho, said the direction of the move was consistent with many schemes’ derisking plans, but the scale of investment was startling given the outlook for gilts.

“There is a move towards matching investments, to reduce the risk of underperforming versus liabilities,” she said.

“Especially as schemes become more mature, it is not surprising that we see a move towards more investments in gilts.”

Schemes may have been hoping for better investment opportunities from a value point of view, Ralston said.

Earlier this year it was reported the London Pensions Fund Authority had sold almost all of its gilt holdings, citing low yields.

Simon Riviere, client director at independent trustee company PTL, said the data were at odds with the sentiment of the schemes he advises, who have been put off by low yields.

“Many schemes have got to the stage where they are looking at an endgame and potentially a move into gilts is seen as a safe haven, particularly [as] equity markets have been volatile recently… however, gilt yields have been pretty low,” he said. “I am quite surprised there has been such a surge.”

Riviere added that many of his schemes are on flight plans to move into liability-matching assets such as gilts, but he has not yet seen a mass movement from equities.

Other schemes have decided either that they do not have a choice but to buy matching assets, or have recognised they might not be able to call this move effectively.

Ralston said: “Some have to come to the conclusion that they need to reduce the risk of being unmatched in their investments and have decided to take a phased approach towards reducing their exposure to inflation and interest rate risk.

“And some schemes have recognised that their ability to judge when is a good time to make that move [has] not been very successful.”

Pension fund money being run through liability-driven investment portfolios, a key avenue for reducing such risks, also grew £74bn to £517bn in 2013.