Merseyside Pension Fund is considering an increase in its allocation to infrastructure, as experts have warned that investors should ensure they have access to the relevant skills and experience.

It has been more than a year since former chancellor George Osborne announced plans to push forward with the pooling of local authority pension funds, outlining the government’s intention for greater investment in UK infrastructure projects.

The ability to source appropriate assets and deals to fulfll a mandate is important; to be actually able to put the allocated money to work in the desired areas within a reasonable time frame

Dan Mikulskis, Redington

Merseyside anticipates an increase in its infrastructure exposure through an investment in the Greater Manchester Pension Fund and London Pensions Fund Authority joint venture, as part of a strategic asset allocation review.

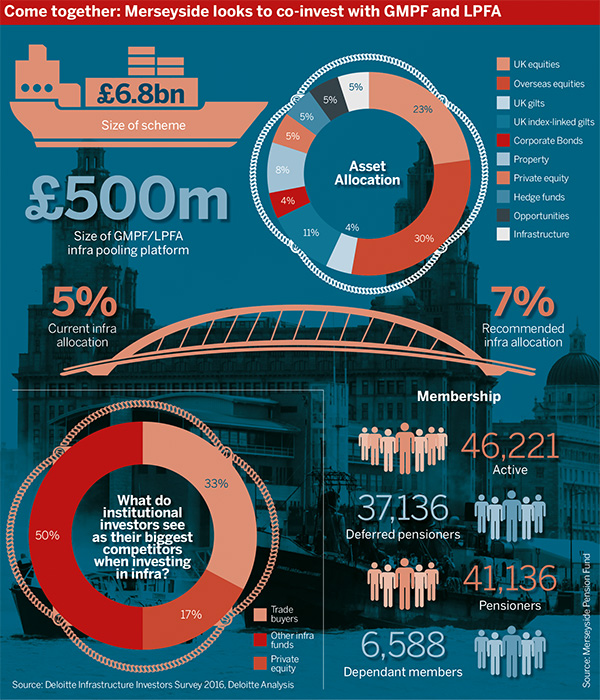

“Taking into account existing infrastructure commitments and investments, an allocation of 2 per cent of MPF’s assets to [GMPF & LPFA Infrastructure LLP] is recommended,” states the agenda for its latest meeting.

GLIL, the £500m infrastructure investment joint venture, was set up in April 2015 by the Greater Manchester Pension Fund and the London Pensions Fund Authority.

Peter Wallach, director of Merseyside Pension Fund, noted: “Strategically, the characteristics of infrastructure fit with the long-term investment horizon of a pension fund.”

He said with bond yields at their present lows, infrastructure has the potential to provide an income stream to pension funds.

The scheme has a 5 per cent target on infrastructure, of which 3.6 per cent is drawn down.

“These assets are performing well,” said Wallach. “Consequently, we are recommending an increase in strategic allocation from 5 per cent to 7 per cent.”

Skills and experience

Dan Mikulskis, head of defined benefit at consultancy Redington, said the challenge with infrastructure is understanding the mix of risks in any given investment and ensuring that the scheme is being adequately compensated in return terms.

“Given the complex and bespoke nature of many of these deals, that requires [a] particular experience and skill set,” he said.

Finding Opportunities

Guy Hopgood, investment research associate at bfinance, said having a sufficient team in place to source deals and operate or manage assets is also crucial.

He noted co-investing can help funds achieve economies of scale and lower fees.

However, Hopgood said infrastructure portfolios are typically fairly concentrated, and a negative impact on just one asset in the portfolio can drag down the performance of the total portfolio.

For local government pension schemes, “it comes down to what projects are available versus what they want”, he said.

Hopgood noted that local authority schemes are looking for assets already in operation that are lower risk. But the government wants “capital being invested in the UK, typically to fund and construct a lot of these projects”, he said.

LGPS funds need to “ensure that they are investing in what’s right for their schemes and their members”, he said.

Dave Lyons, head of public sector investment consulting at Aon Hewitt, said co-investing in infrastructure is “a good way forward”.

For most LGPS funds looking to this asset class, “it’s going to be a case of partnering up with other funds who perhaps have a little more experience”, said Lyons.

He explained that collaborating enables schemes to share the necessary governance and oversight, due diligence and investment skills needed to invest in illiquid markets successfully.

Investing locally

Lyons noted there is a lot of interest among LGPS funds to invest in their local areas. “This is, however, fraught with potential challenges,” he cautioned.

In-house management and infrastructure dominate LGPS pooling debate

As the pooling of the Local Government Pension Scheme progresses, some funds have warned of the risks of in-house management and questioned whether infrastructure investment is necessarily a good bet

When undertaking a more direct, local, impact-driven investment, funds need to ensure that it meets any primary objectives in terms of diversification or a different source of expected real return.

“There is also, of course, the potential for reputational risk,” Lyons said, if the investment does not work out. “A poor outcome in their local area might not be the kind of publicity or outcome that they would want to be associated with.”