Schemes hunting for cash flow in a record-low gilt yield environment are turning to corporate bonds, emerging markets and active management of their debt portfolios, a study has revealed.

Mercer’s European Asset Allocation Survey found that UK schemes have continued the trend of steady outflows from equities, looking to alternatives to generate their returns.

The survey reflects around €930bn (£736bn) of European assets, 56 per cent of which were controlled by UK institutional investors. Several key statistics were disaggregated to show UK-specific trends.

Any negative returns together with the effect of that negative cash flow will mean that a higher level of return is needed

Michael Chatterton, LawDeb Trustees

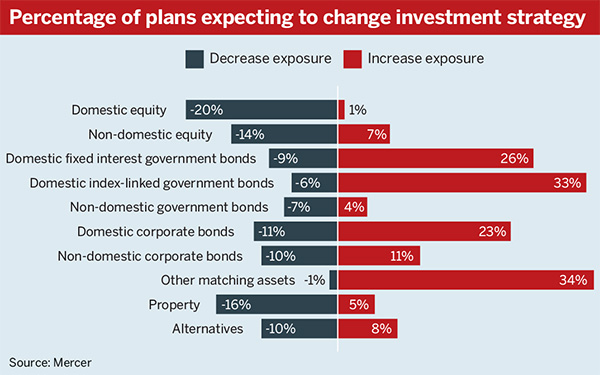

British plans’ bond allocations remained at the 2015 level of 48 per cent, although separate research led by JLT Employee Benefits showed huge inflows to the asset class from FTSE 100 defined benefit schemes.

Standard Life topped the switch tables, increasing its bond allocation by 28 per cent during 2015.

Bonds still the answer to cash flow demands

Ten-year gilt yields hit record lows on Monday, moving below 1.2 per cent for the first time. Some have suggested that the volatility in bond markets is caused by uncertainty over the outcome of the EU referendum.

But Nathan Baker, principal at Mercer, said higher-yielding debt will still prove attractive to an increasing number of UK schemes that are cash flow-negative.

“In the UK specifically that’s nearly half of schemes now, I’d have thought,” said Baker. He expected the number of schemes pursuing cash flow-driven financing strategies to increase steadily from its current level of 4 per cent.

“It’s going to first off be about understanding the liability cash flows and how they are going to lay out, and then to essentially match those where you can with cash flows from the asset side,” he explained.

Mercer’s survey also showed that pension investors were prepared to maintain their commitments to emerging market and private debt, despite what the consultancy highlighted as poor performance over the past few years.

Baker said a growing number of schemes across Europe are adopting multi-asset credit strategies in order to mitigate the risks associated with investing in higher-yielding debt.

Focus returns to alpha

Negative cash flow will also put increasing pressure on trustees to manage downside risk, according to Michael Chatterton, managing director at LawDeb Pension Trustees.

“Any underperformance, any negative returns – together with the effect of that negative cash flow – will mean that a higher level of return is needed to put the scheme back into the situation it was in before that period,” he said.

The complexities of multi-asset credit strategies, and the higher risks associated with higher-yielding debt, could see schemes relying more on active managers.

While recent years have seen schemes shy away from the costs of active equity management, manager outperformance may still have its place within successful strategies.

“Alpha and manager skill is starting to show itself in a different sort of way,” he said. “You might not have active equity, but you would almost certainly have active corporate bonds.”

Breaking out of ‘herd mentality’

Roger Mattingly, director at PAN Trustees, urged schemes to seek tailored solutions to the volatility of the current economic climate.

He said the industry’s previous commitment to sovereign debt despite decreasing yields was testament to its “instinct to move with the herd”.

“There’s obviously logic in terms of liability matching and liability-driven investment, but there comes a time when it’s not good value,” he said.

Schemes should instead question whether their consultants are adding value, he said, and play “devil’s advocate” to ensure the advice they receive is tailored to their needs rather than generic to the industry.