Intercontinental Hotels Group has increased its default pension contributions to 2019 minimum levels a year early, after a multi-pronged member communications exercise last year sought to persuade employees to increase saving levels voluntarily.

Auto-enrolment minimum contributions for employees rose to 3 per cent from 1 per cent in April this year, while employer contributions went up to 2 per cent from 1 per cent.

You’ve got to make it simple for people to take the action that you want them to take

Karen Bolan, AHC

In April 2019, contributions will increase again – to 3 per cent for employers and 5 per cent for staff.

While these increases will help people put more into a pension, there are concerns that some savers will opt out, raising questions over how employers and providers can maintain the savings habit.

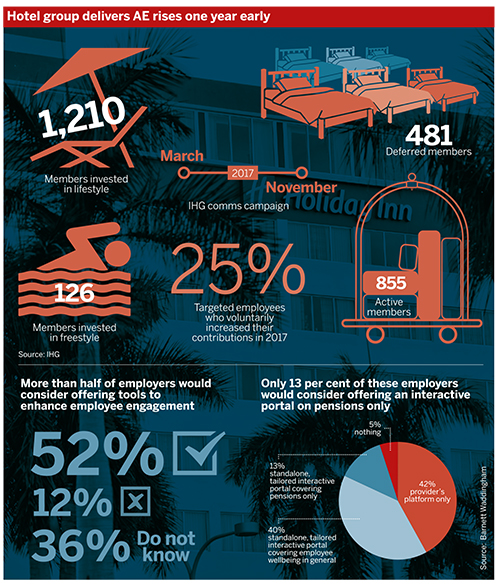

IHG promotes pensions with comms campaign

Last year, the trustees of the IHG UK Defined Contribution Pension Plan decided to carry out a communications exercise to encourage staff paying in 1 per cent or 3 per cent of their salary to voluntarily increase their contributions.

Ben Hawley, pensions manager, said the scheme engaged with a third-party company who has an online application designed to highlight the affordability of increased contributions and the positive impact on potential retirement outcomes for staff.

“The app demonstrates the tax relief employees receive on their own contributions, the increased employer contributions they get by increasing their own and the increased likelihood of achieving the income in retirement that they desire,” he said.

Alongside the app, the scheme also ran a series of communications. These included several emails to introduce the app and to invite employees to face-to-face seminars, a webinar and one-to-one telephone consultations. The campaign ran from March to November 2017.

“By definition, the group of employees we targeted were the least engaged in terms of pensions, as most of them had been automatically enrolled into the plan,” said Hawley.

“However, the employees who did respond gave very positive feedback on both the app and the presentations. The majority of those employees who used the app went ahead and increased their contributions,” he added.

Overall, 25 per cent of the group of employees that were targeted voluntarily increased their contributions in 2017.

Group jumps ahead of AE curve

IHG members can choose to pay a core contribution of 3, 4 or 5 per cent and the company matching contribution is a multiple of the employee contribution.

There was also a 1 per cent contribution band that was introduced when IHG staged in 2013 specifically to meet the auto-enrolment requirements at that time.

This contribution band has been removed, in line with the 2018 minimum increases. Rather than wait another year to implement more increases, IHG decided that contributions in the scheme would be brought up to 2019 minimum levels by default immediately.

From April 2018, all staff who were eligible workers paying contributions of 1 per cent or 3 per cent were increased to 4 per cent, and new staff are auto-enrolled with a 4 per cent contribution rate. The lowest matching multiple at the company is 1.5 times the employee contribution, so this will meet the 2019 requirements.

If they feel they cannot afford to pay 4 per cent, members can opt down to 3 per cent as an alternative to opting out altogether.

“We have issued further communications this year, including posters in the offices and individual emails, to all employees who were due to be automatically moved up to the 4 per cent contribution rate,” said Hawley.

He added: “To date, only a very small number of employees have decided to opt out or opt down to the 3 per cent contribution level; and a similar number have chosen to increase their contributions to the 5 per cent matching level.”

Keep communicating to engage staff

Jonathan Parker, director at consultancy Redington, said that increasing minimum contribution rates early depends on affordability, both from the perspective of the employer and members.

That is why it is important for a scheme to know its membership well enough to understand whether that pace of increase will be welcome or not.

For companies who have decided to “bite the bullet now… they put in place a six to nine-month programme of communications with staff” to make them aware, give them time to prepare and prevent opt-outs.

The employer can also emphasise the long-term tax and contribution benefits of a pension scheme to staff.

The types of communication used to pass on these messages depend on the membership, but usually a mix of methods is most effective, according to Parker.

A big organisation may have a very large and diverse workforce in terms of age, financial knowledge and level of pension savings, meaning a one-size-fits-all approach may not work.

“The reiteration of that message through whatever medium you choose, on a regular basis, is absolutely key,” Parker added.

Combine pensions with monthly pay info

Some companies may have a good idea of how best to communicate with employees, drawing on previous experiences. However, in many cases, Parker said that companies should adopt a trial and error approach.

“An approach that we found worked very well with one particular organisation was including very short and sweet nuggets of information alongside monthly payslips,” he added.

This is something that most employees are likely to look at monthly, and so “it starts to hammer home that message”.

Karen Partridge, head of client services, UK and Australia, at communications specialist AHC, said communications should be done “in a campaigned approach, so that you do get that joined up thinking and joined up messaging”.

She said that “an app itself is not the panacea”. A successful campaign requires “thinking strategically, thinking [about] what you want people to do as a result of every piece of communication that you send out”.

An app can boost engagement, but getting members to actually use it needs careful thought, Patridge noted.

“It needs to be something that you’re going to all the time… you’ve got to give them reasons to go there,” she said.

For example, if employees can access their pay information via the app, that would encourage them to visit it often.

The effect of employer contributions

Once employees access an app, “you’ve then got to make it simple for people to take the action that you want them to take,” said Karen Bolan, head of engagement at AHC.

She pointed out how employer contributions also play a significant role in encouraging people to save more.

“If that company match amount moves, then members are quite likely to move their own contribution rate as well,” she said.

A Royal London survey of 1,500 25 to 34-year-olds, conducted in 2017, asked respondents if they would stay in their workplace pension if their contributions increased automatically.

If total contributions increased to 5 per cent, with a 3 per cent contribution from their employer and a 2 per cent contribution from them, nearly three quarters said they would continue to save in their pension.

If the contributions were increased to 8 per cent, but were matched with 4 per cent from the employer and 4 per cent from the worker, an even larger proportion of respondents said they would keep saving.

However, if total contributions increased to 8 per cent, with the employee paying 5 per cent and the employer 3 per cent, then those prepared to continue to save dropped to nearly two thirds, according to the research.

“If you’re… still quite a paternalistic employer, and you want to encourage your members to actually pay more into the pension scheme, then certainly increasing your employer contributions can be a good way to drive that action,” Bolan said.