Retailer John Lewis has agreed a new recovery plan with the trustees of its defined benefit scheme after a large reduction in the funding deficit, due in part to a change in inflation indexing.

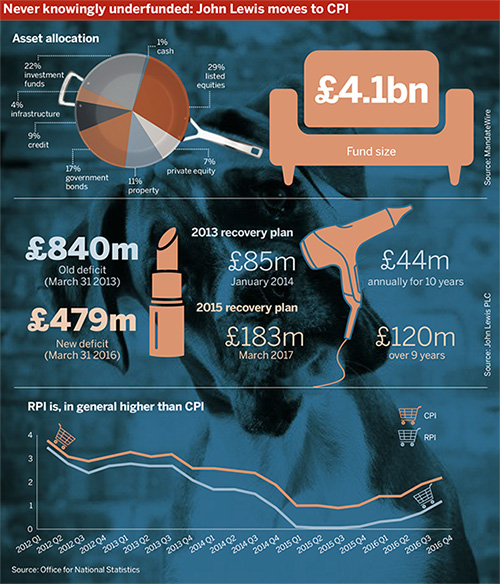

The scheme carried out a triennial valuation dated March 2016, showing a deficit of £479m down from £840m in March 2013, prompting discussions about the recovery plan.

Trustees find it a very difficult decision when they have been telling members for years they will get RPI increases and funding for RPI increases

Glyn Bradley, Mercer

In an update, the company said the reduction was due to “payment of deficit contributions, a change in allowance for discretionary pension increases, and excess investment returns, partly offset by a reduction in the real discount rate”. It did not comment on which assets had driven the outperformance.

Following the previous valuation, John Lewis agreed to a recovery plan consisting of an £85m one-off payment followed by £44m annually over 10 years.

However, the company issued a £300m bond in December 2014, using the proceeds to prepay almost seven years of contributions up front.

The new plan includes £303m of cash contributions, £183m of which are due before the end of March 2017. The remaining £120m will be paid over the nine years to March 31 2026.

A spokesperson for the scheme said the roughly £182m discrepancy between the size of the deficit and recovery plan was “expected to be met by investment returns on the scheme’s assets”.

The “change in allowance for discretionary pension increases” mentioned in the scheme’s update was a switch to the consumer price index from the retail price index for annual increases to different sections of the scheme.

The spokesperson explained: “The Partnership announced that the annual increase for pension built up before April 6 1997 is, in the future, expected to be calculated using CPI inflation (capped at 2.5 per cent) instead of RPI inflation (capped at 5 per cent). This change has been implemented to make sure that the John Lewis Pension is affordable and fair to past, current and future partners.”

Changing indexation

RPI was traditionally the favoured method of indexing DB pensions for inflation, but it has declined in popularity in recent years.

CPI and RPI are calculated differently, both in terms of the ‘basket of goods’ on whose prices the calculations are based and the mathematical formulae used to calculate the increases.

The upshot, said Glyn Bradley, principal at consultancy Mercer, is that with CPI “you’d be expecting one per cent less per year” in increases.

Because of this, the cost of future liabilities is lower and therefore CPI is often more attractive to employers, while RPI holds greater appeal to savers.

“Trustees, we find, are caught in the middle,” said Bradley. “They aren’t all rushing one way to the other. They find it a very difficult decision when they have been telling members for years they will get RPI increases and funding for RPI increases.”

Back in 2014, the government installed CPI in the Local Government Pension Scheme for indexing pensions in payment, where before it had been RPI for pre-2011 increases and CPI thereafter.

'Rules lottery' continues after Court of Appeal's RPI/CPI judgment

Trustees of the Barnardo Staff Pension Scheme will not be allowed to provide indexation of benefits in line with the consumer price index, according to a Court of Appeal decision.

However, whether or not private schemes are allowed to follow suit has been the subject of numerous legal cases, as it depends on specific phrasing in the trust deed and rules.

Ruth Bamforth, senior associate at law firm Walker Morris, said: “The question is always, ‘Can you move from RPI to CPI?’ It very much depends on how your rules are written. It’s pot luck. Some rules write [the type of indexation] out in glorious technicolour and some refer to legislation.”

The rules can be fickle, and changes are considered on a case-by-case basis. In a recent case involving children’s charity Barnardo’s, the High Court ruled the scheme was not allowed to switch as RPI was still being published as an official index.

However, another case involving retail company Arcadia Group found the power to switch indexing was jointly vested in the employer and trustee, and that rules in the 1995 Pensions Act did not preclude a move to CPI.

Bamforth said the issue of RPI versus CPI is expected to be addressed in the government’s forthcoming green paper on DB.