The West Midlands Pension Fund has agreed to divest from South Korean arms manufacturer Hanwha Corporation after years of sustained pressure on the company from institutional investors across the globe in relation to cluster munitions.

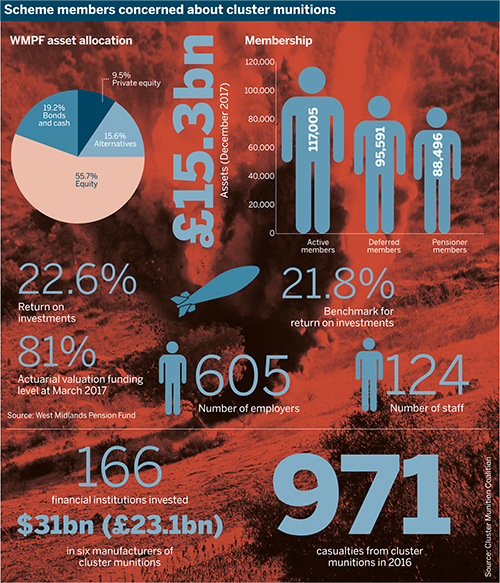

Between 2013 and 2017, 166 financial institutions invested $31bn (£23.1bn) in six manufacturers of cluster munitions, according to Dutch campaign organisation PAX.

In December, the £15.3bn fund agreed to deselect Hanwha from its internally managed passive equity portfolio, worth around £4.5bn, with the stock making up less than 0.01 per cent of the fund’s assets under management.

The move came after members had written to the fund expressing concerns over Hanwha’s connections with cluster munitions production.

According to the Norwegian ministry of finance, which announced on January 11 2008 that it had also excluded Hanwha from its $1tn (£776.3bn) Government Pension Fund Global, the company confirmed by letter that it produced air and ground-delivered cluster munitions at that time.

It is unclear whether the company still manufactures the controversial weapons.

The Local Authority Pension Fund Forum – a shareholder engagement group representing 75 funds with more than £230bn in combined assets, which includes the WMPF – has written to Hanwha twice via engagement company Pensions and Investments Research Consultants expressing concerns over its links to cluster munitions.

People tend to assume that their pension fund would not dream of investing in something like this

Catherine Howarth, ShareAction

PIRC obtained a response in August 2017 but would not disclose the content of the letter. Hanwha could not be reached for comment.

Cluster munitions are banned under the Convention on Cluster Munitions, which was opened for signature in 2008 and came into force on August 1 2010. The UK, along with 119 other states, is committed to the goals of the convention, according to the Implementation Support Unit of the Convention on Cluster Munitions.

In the UK, the direct financing of cluster munition production became illegal following the introduction of the Cluster Munitions (Prohibitions) Act 2010. The act did not, however, prohibit indirect investment.

South Korea is not a signatory to the Convention on Cluster Munitions. As a South Korean manufacturer, Hanwha is therefore not bound by the convention.

The WMPF joins the ranks of large institutional investors, such as mastertrust Nest and the Norwegian Government Pension Fund Global, that exclude from their portfolios companies linked with cluster munitions.

The Cluster Munition Coalition recorded 971 casualties linked to cluster munitions in 2016. In its annual Cluster Munition Monitor, the organisation says: “It is certain that this number does not capture all actual casualties and therefore the real number is most likely higher.”

Members have held concerns over Hanwha

Whatever Hanwha’s current stance on cluster munitions, its historical association with the weapons has led members to campaign for divestment.

At its December 2017 meeting, Michael Marshall, then responsible investment officer for the West Midlands fund, listed a number of arguments in favour of divestment from Hanwha.

According to minutes from the meeting, he argued that “the deselection of this particular stock at this particular time is not expected to cause significant financial detriment” and “that there is likely to be portfolio reconstruction in the near term, which represents a rare opportunity to execute the deselection.”

He added: “Scheme members have expressed ethical concerns regarding Hanwha Corporation.”

The WMPF declined to comment on the timing of its divestment from the South Korean manufacturer.

Hanwha initially failed to respond

The PIRC first sent a letter on behalf of the LAPFF to the chief executive officer and the chair of Hanwha in 2014 raising concerns over cluster munitions.

It also expressed misgivings over a “lack of dialogue with shareholders”, according to a PIRC spokesperson.

The spokesperson said: “Subsequent to some institutional investors disinvesting from the company, the forum was exploring the extent to which Hanwha has stopped producing and selling cluster munitions, or intends to do so, and evidence of policies or practices that prevent or mitigate the effects of cluster munitions.”

A second letter was sent in April 2017 after the company failed to respond to the LAPFF’s first correspondence.

In August 2017, a company representative provided a written response setting out Hanwha’s position on cluster munitions, but would not commit to a meeting with the forum.

Fund has engaged with other companies

The WMPF has engaged on this issue with several companies. It asked the LAPFF to assess whether certain aerospace and defence companies were producing or selling cluster munitions

Nine companies were contacted in November 2014. Lockheed Martin, Textron, Singapore Technologies and Alliant Techsystems – which has since merged its aerospace and defence groups with Orbital Sciences Corporation, leading to the creation of Orbital ATK. All responded to the letters, and the WMPF later decided not to pursue divestment in all four.

Committee minutes from a meeting that took place on December 9 2015 state that the four companies “had explicit references to the production of cluster munitions on their websites and/or in their promotional materials”.

“The engagement program of the four companies was completed in November 2014 and based on its findings, the pensions committee decided to not exclude the companies from its investment portfolio,” the minutes continue.

According to the LAPFF, Singapore Technologies ended its production of cluster munitions in 2015, with the company citing the forum’s engagement as a factor in its decision. In 2016, Textron announced in a Securities and Exchange Commission document that it no longer produces cluster munitions.

Meanwhile, a spokesperson for Lockheed Martin confirmed the company “does not develop or produce cluster munitions as defined in the 2008 Convention on Cluster Munitions.” Orbital ATK did not respond to a request for comment.

Sometimes, exclusion is the only way

In addition to receiving written concerns from members, the WMPF also faced pressure from local campaigners, including the Coventry Justice and Peace Group, which began campaigning for divestment in 2014.

Some environment, social and governance proponents have made the case for remaining engaged with companies to help them achieve sustainable long-term profits, using voting rights where necessary.

But Andrew Smith, spokesperson for activist organisation Campaign Against Arms Trade, thought it unlikely that investors would be able to influence company policy at arms manufacturers with voting rights.

“We’ve never seen any evidence of an arms company changing its ways in order to attract investment from local authorities,” he said.

“I certainly don’t believe that an arms company... is going to cease the production of cluster bombs because they get asked to by any local authority in the UK,” Smith added.

A good way to engage with members

In December 2017, the committee agreed to write to all members who had contacted the fund concerning Hanwha.

Catherine Howarth, chief executive of campaign group ShareAction, predicted that the divestment would be popular with the membership. “People tend to assume that their pension fund would not dream of investing in something like this.”

She said there is “a tiny, tiny number of companies involved in the manufacture of controversial weapons, like cluster munitions, in the world, so excluding them is completely irrelevant from a financial risk point of view,” adding that “it’s an ethical stand”.

I’m pleased my pension fund was proactive in contacting Hanwha

David O'Sullivan, WMPF member

David O’Sullivan, a policy officer at ShareAction who is also a member of the WMPF, said it was “stomach-churning” reading where his pension had been invested.

“I’m pleased my pension fund was proactive in contacting Hanwha,” he said. “Putting money into weapons proscribed under an international treaty is clearly not a sound investment... I’m glad West Midlands Pension Fund chose to divest.”

Investing passively for the greater good

However, exclusion can come at a price, as the Norwegian government found. A 2017 report published by Norges Bank Investment Management described the exclusionary policy on arms and tobacco’s drag on the Government Pension Fund Global’s performance.

“The product-based exclusions have reduced the cumulative return on the equity index by around -2.4 percentage points, or -0.10 percentage point annually. Both the exclusion of tobacco companies and certain weapons manufacturers have reduced returns,” the report reads.

While passive investment has its plaudits, reconciling the passive style with ESG objectives presents a range of difficulties for investors.

Where active managers normally make use of their own research, passive providers have been accused of being overly-reliant on third-party sources of ESG data.

ESG investing has little to do with ethics

Carolyn Saunders, head of pensions and long-term savings at law firm Pinsent Masons, argues that trustees should focus on the risks to investment performance that are financially material.

Richard Butcher, managing director at professional trustee company PTL, recognised the constraints on ESG investment imposed by passive management.

“The difficulty you have is how you can exercise leverage over a company [where] you want to change their social profile. Your principle use of leverage – disinvestment – is no longer available to you,” he said.

“You might do that through voting down the directors’ pay package, for example, but you are more constrained,” he added.